Summary

MakerDAO, one of the most long-standing and successful crypto projects in decentralized governance, development, and operations, has entered the “Endgame Plan” phase. It aims to reduce Maker’s operating costs and isolate risks by establishing several SubDAOs, stripping new features and products based on the Maker system, and to self-govern, self-profit, and loss, including potential new coin offerings. This move is expected to make Maker into an ecosystem similar to that of Layer 1s, allowing “all things to grow” and enhancing the sustainability of its increasingly complex system.

A new SubDAO composed of former MakerDAO members, including core developers and its Chief Growth Officer, will release the Spark lending protocol based on Aave V3 code in April this year. Spark is expected to unlock more value for the over $8 billion collateral in Maker’s treasury, theoretically combining with the low-cost D3M lending module and PSM minting pool within the Maker system to form powerful synergistic effects, providing the most competitive and relatively stable interest rates for $DAI.

The “matrixing” of DeFi has become a trend, with some old-school DeFi applications developing more native nested products based on user assets or liquidity advantages. For example, Curve has announced crvUSD, Aave plan to launch $GHO, and Frax has launched its Lend pool. However, compared with the difficulty of Aave/Curve in growing its market share of its GHO/crvUSD stablecoins, it is much easier for Maker to expand its lending business.

The launch of Spark represents the beginning of a major transformation for the Maker ecosystem. One of the most significant marginal improvements is the $MKR token, and the valuation model needs to shift from being viewed as a single project token to an ecosystem token similar to that of a permissionless blockchain. The $MKR token, which originally granted only governance rights, now has a scenario for staking the token which may provide $MKR stakers 12–37% APY, while ecosystem applications will effectively expand Maker’s balance sheet. Under bear and base-case scenarios, it could bring an additional $2.75–12 million in annual revenue to Maker, which in turn increases the amount of $MKR burned by 1–3 times.

Spark Protocol

On February 9, 2023, part of MakerDAO’s core team❶ created Phoenix Labs, which is dedicated to developing new decentralized financial products geared towards expanding the Maker ecosystem. The creation of Phoenix Labs came after MakerDAO’s founder proposed the “Endgame Plan” last June, stating that the project needed to continue expanding while maintaining maximum flexibility.

Spark Protocol is the first protocol developed by Phoenix Labs. It is a money markets protocol that facilitates borrowing using the $DAI stablecoin and other mainstream crypto assets as collateral. As the first protocol to illuminate Maker’s new DeFi matrix, the name “Spark” coincidentally conveys the Chinese proverb “a single spark can start a prairie fire.”

The protocol is built on Aave V3 code, whose lending business has been battle-tested by the market over a long period. Users can use highly liquid assets such as ETH, WBTC, and stETH as collateral to borrow corresponding assets based on its interest rate model. In theory, it will combine with Maker’s low-cost D3M lending module and the PSM casting pool, which is nearly 100% capital-efficient for stablecoins, to form a strong synergistic effect, providing the most competitive and relatively stable interest rates for $DAI across the entire market.

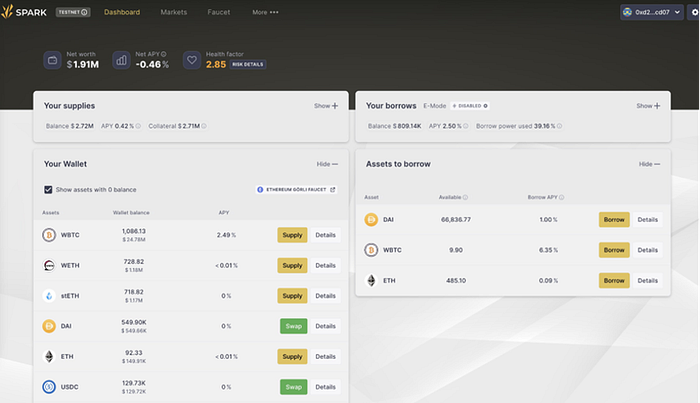

Figure 1: Spark Beta Webpage

The Spark team has stated that 10% of the profits earned from its $DAI market will be distributed to Aave over the next two years only once the $DAI lending market reaches $100 million. A proposal for this has already been initiated on the Aave forum.

Product Advantages of Spark Protocol:

Proven Codebase

As the codebase is based on the mature codebase of Aave, its code has been battle-tested and is highly secure. Additionally, like aTokens, depositors can also receive tokenized versions of their positions (spTokens). spTokens can be moved and traded like any other crypto asset on Ethereum, thus improving capital efficiency.

Low-Interest Stable Rate Lending

Spark Lend can directly utilize Maker’s credit line, known as the Dai Direct Deposit Module (D3M)❷, allowing users to theoretically borrow any amount of Dai at a slightly higher❸ interest rate than the Dai Savings Rate (DSR), currently at 1% (with an initial debt ceiling of 200 million $DAI).

High Capital Utilization Efficiency of ETH Assets

Spark Lend also introduces Aave V3’s e-Mode module, allowing ETH assets to be borrowed with LTV ratios of up to 98%. For example, pledging wstETH can allow for borrowing up to 98% of ETH, increasing capital utilization efficiency.

Double Oracle Price Feed for Increased Manipulation Resistance

Spark may use both ChronicleLabs (formerly Maker Oracles) and Chainlink as data sources to provide on-chain prices. These two data sources will be checked through three steps: TWAPs (time-weighted average prices), signed price sources, and circuit breakers, to ensure prices cannot be manipulated.

Fair Launch

Protocol token distribution is entirely through liquidity mining, with no pre-allocation❹, providing a fair distribution mechanism that can attract more people to join the community and increase consensus and value. The project also believes that Spark Protocol needs to compete in a fair environment to win support from SubDAO and to be fully accepted as a product.

100% Backed by MakerDAO

Spark is not a typical “third-party” protocol. Though it is being developed by Phoenix Labs, it is fully owned by Maker Governance (including all smart contracts, trademarks, IP, etc). This means that in the event the protocol encounters any insurmountable difficulties, Maker will likely step in to provide support.

Three initiatives to help DAI become a better “world currency”:

Maker’s mission is to create a “fair world currency”. But so far, compared to the $70+ billion market cap of USDT, DAI’s market cap of $5+ billion is relatively small. So how can DAI expand and ultimately surpass centralized stablecoins?

The launch of the Spark Protocol indicates three directions for the future development of Maker’s products, all aimed at increasing the minting volume of DAI and reducing its usage costs:

- Integration of Internal D3M and PSM Features

Spark Lend has integrated Maker’s internal D3M❺ and PSM❻ modules to provide liquidity for the stablecoin DAI. The most significant advantage of D3M is that it allows the secondary market to directly mint DAI, eliminating the need for primary minters to first mint DAI in Maker and then deposit it into secondary market applications. This merges the two layers of excess collateral into one layer, improving the capital efficiency of DAI.

The initial plan is to provide $300 million of D3M liquidity to Spark Lend, with $200 million as a hard cap in the first phase and $100 million as buffer funds. This scale limit will be adjusted based on the actual market lending rate performance.

In addition, the Spark Lend front-end will support MakerDAO’s PSM and DSR. This promotes the use of DAI from the demand side as USDC holders can directly convert USDC in the PSM into DAI through Spark Protocol’s website and earn deposit interest through DSR.

For example, under normal circumstances, lending out 1 DAI in Aave’s lending market requires two layers of collateral: about $1.5 of Aave collateral❼ and $1.5 of collateral in the Maker vault. Without considering circular borrowing and lending, this common scenario actually requires $3 of asset collateral. However, after integrating D3M and PSM, lending out 1 DAI on Spark only requires $1.5 of collateral (or $1 of whitelisted stablecoins such as USDC), greatly improving capital efficiency.

2. Entering the LSD Market through EtherDAI

Spark Protocol will bootstrap the use of EtherDAI, a liquid staking derivative based on ETH (ie. Lido’s stETH). Users can wrap stETH as ETHD and use it as collateral to borrow DAI.

Maker governance will have backdoor access to the ETHD collateral and may incentivize liquidity by setting up short-term liquidity mining programs for ETHD/DAI on Uniswap. On the other hand, the stability fee for the EtherDAI Vault may be set to zero to encourage demand for the EtherDAI Vault.

Furthermore, with the Ethereum Shanghai upgrade, which will provide over 4% base yield for ETH assets, a large-scale migration of ETH assets is inevitable. Spark’s support for liquid staking derivatives (LSD) wrapped tokens will prevent TVL from shrinking and may even attract more funds into the protocol through income stacking, potentially reducing its reliance on USDC.

More importantly, TVL represents the locked value of funds in the protocol. As TVL increases, so does liquidity, availability, and potential revenue for the protocol, primarily from the interest rate spread between lenders and borrowers.

3. Maker + Spark = The market’s lowest and predictable interest rate

The introduction of Spark Protocol will enable Maker to better control DAI supply based on market demand, interacting directly with its secondary market to provide better rates for its users and increase DAI supply.

Specifically, during DeFi booms, lending rates often skyrocket. This causes users to pay higher-than-expected borrowing rates and negatively impacts the supply-demand market for DAI. D3M will influence the main DAI lending market (Spark) by stabilizing DAI interest rates. When there is high market demand for DAI, Maker can increase Spark’s hard cap for DAI minting and its supply to lower its interest rate. Conversely, if demand is weak, DAI liquidity will be removed from Spark to increase its interest rate.

Overall, maintaining the cheapest and predictably fluctuating borrowing rate for DAI in the stablecoin “battlefield” is a key competitive advantage in increasing its usage. The D3M funding pool can achieve relative stability in DAI borrowing rates and offer the most competitive rates across the market.

Current Revenue and Expense Analysis of the MakerDAO Protocol

MakerDAO’s current expenses exceed $40 million per year. Without aggressive investment in RWAs, the protocol would face a net loss of $30–40 million. Therefore the founder’s proposal for an “Endgame Plan” is centered on increasing revenue and reducing expenditures.

Revenue

MakerDAO’s current sources of revenue mainly come from four areas:

Stability fee income from over-collateralized Vaults, i.e. interest on minting/borrowing DAI;

Liquidation revenue from under-collateralized asset liquidations;

Stablecoin trading fees from PSM;

Returns on RWA (real-world asset) Vaults.

The stability fee charged on crypto asset Vaults used to be the protocol’s most significant source of revenue, but currently income from RWAs has become its largest revenue source.

Expenses

Protocol expenses mainly include employee salaries, growth/marketing expenses, with the largest proportion being engineer salaries to maintain the protocol’s core.

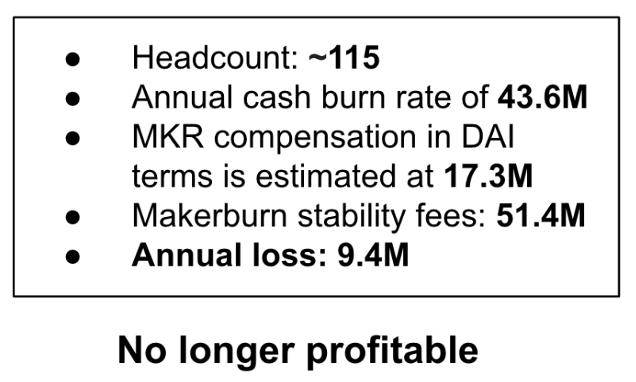

Data released by MakerDAO co-founder Rune Christensen in June 2022 showed that MakerDAO’s annual stability fee revenue was about $51.4 million, but the cost to maintain the protocol was $60.9 million, including $43.6 million in cash flow and $17.3 million in $MKR priced in $DAI. Its cost has exceeded the protocol’s revenue, resulting in a net annual loss of approximately $9.4 million.

Figure 2:MakerDAO Profitability Breakdown

One major reason for the protocol’s significant losses is: 1) the bear market environment has led to a sharp decrease in protocol revenue; 2) team expenditures are generous; 3) governance redundancy. The existing governance process is complex, requires extensive personnel participation, and has a long governance cycle. All of which constrain the development speed of new product features.

Therefore, Rune Christensen proposed the concept of the Endgame Plan, which we will detail in the following text. The plan includes a solution to the current protocol’s revenue shortfall, which is to increase the growth of RWA (real-world assets).

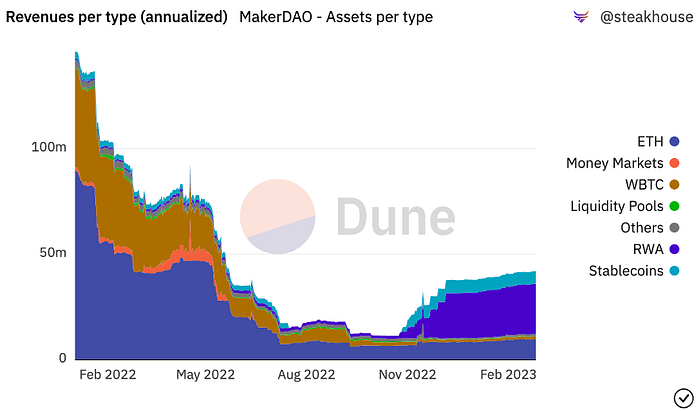

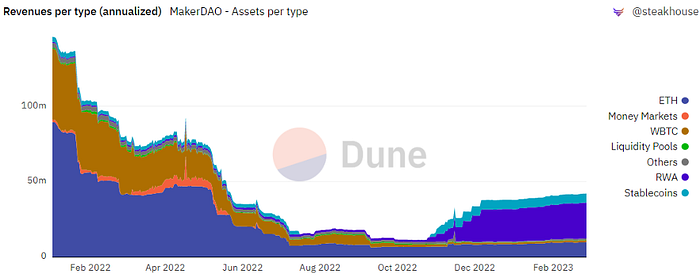

Figure 3:MakerDAO Revenue Breakdown

From the above chart, we can see that: 1) ETH Vault was a significant source of revenue for MakerDAO before November 2022; 2) After November 2022, RWA (real-world assets) Vaults became the largest source of revenue for the MakerDAO protocol.

The RWA Vault refers to investments in off-chain financial markets, mainly bonds and mortgages. Because RWA collateral can bring higher stable fee income to MakerDAO, it has indeed brought higher income to the MakerDAO protocol as expected. Based on its current investment of $696 million, it is expected to generate over $26 million in interest income, accounting for more than 40% of Maker’s total revenue.

However, on the other hand, there is a relatively large risk for RWAs to be confiscated by regulators. Therefore, the ‘Endgame Plan’ proposes a series of strategies to mitigate RWA regulatory risks: under mild regulatory conditions, Maker will prioritize maintaining a 1:1 anchoring strategy with the US dollar and will not restrict RWA exposure to generate as much revenue as possible. The founder assumes that future regulatory policies will become increasingly strict, so Maker’s exposure to RWA will not exceed 25% and may de-peg from the US dollar when necessary. The ultimate stance is to maintain maximum flexibility and survivability of DAI, to no longer allow easily seizable RWAs as collateral, and to not have a major currency act as a price reference.

Relying on RWA income is not a viable long-term solution. To maximize the sustainability of the Maker protocol, it is necessary to expand Maker’s sources of revenue as much as possible, optimize its system’s organizational structure, and aim for increased revenues & reduced cost expenditures.

The Endgame Plan, Everything Grows.

In order to better understand the upcoming major changes in the Maker ecosystem and the improvement of the supply-demand relationship of the $MKR token, it is necessary to first understand the “Endgame Plan”. Although the plan involves many discussions regarding regulation and politics, it essentially aims to make Maker into a Layer 1-like ecosystem that allows for the “growth of all things”.

The Endgame Plan was first proposed by Rune in June 2022 and has undergone at least three versions of full-scale discussions on the governance forum. It is a structural reorganization plan for MakerDAO that aims to make it a decentralized, self-governing DAO (decentralized autonomous organization) to better meet the needs of its stablecoin DAI users. The plan includes four main components:

● Establishing complete decentralization for MakerDAO

● Improving DAI liquidity and stabilizing its interest rate

● Enhancing protocol sustainability and reducing system risks

● Improving decentralized governance and DAO operations

To simplify the complexity of governance, Maker will create a series of self-sustaining DAOs called MetaDAOs❽. Rune compared Maker Core to L1 Ethereum, which is secure but slow and costly to operate. MetaDAO is an L2 solution that can operate quickly and flexibly while also obtaining security from the L1. Through implementation of MetaDAOs, MakerDAO can focus more on its primary goal of issuing and stabilizing its stablecoin DAI. Additionally, MetaDAOs can provide governance support for other projects in the MakerDAO ecosystem.

The so-called MetaDAOs will modularize the Maker protocol, with each MetaDAO being a small community that can have its own tokens and treasury. The core value proposition of MetaDAOs is isolation, risk reduction, and parallelization of Maker’s highly complex governance processes.

Figure 4:The role of MetaDAOs in the Maker Ecosystem

MetaDAOs will be classified into three types:

Figure 5:Types of MetaDAOs

Maker Core retains all the essential and irremovable components of the Maker protocol to fully function and achieve its goal of generating and maintaining DAI. Each type of MetaDAO around the Core has its own function, which determines its interaction with Maker Core:

Governor (also known as Facilitator) is responsible for organizing decentralized staff management, on-chain governance, engineering, protocol management, and brand management of Maker Core;

The creator focuses on the growth of the Maker ecosystem and the development of new features, such as the Spark team;

Protector will manage RWA Vaults, focusing on real-world assets and protecting Maker from physical and legal threats against its real-world collateral.

Similarly, MetaDAO has a governance process similar to Maker Core, using the deployment of new ERC-20 tokens for governance, which can overcome the current single-threaded problem in Maker’s governance process and allow MetaDAO to execute in parallel, speeding up the governance process.

However, MetaDAO runs its governance process on top of Maker Core’s governance infrastructure, meaning that MetaDAO voters pass governance signals that are bundled and executed in Maker’s Executive Vote. This means that MKR holders can act as an “appellate court” and have actual control over the protocol of MetaDAO through MKR voting.

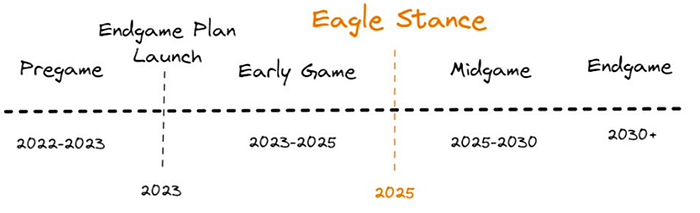

The Endgame Plan is divided into four stages, with the Pregame stage expected to be launched within 2023, including the construction of ETHD, the launch of MetaDAO, and the initiation of liquidity mining, among others.

Figure 6:Endgame Plan Roadmap

Spark Protocol will be the first MetaDAO, which is expected to launch in April 2023. It is currently undergoing mainnet deployment and a series of branding initiatives. In the second half of this year, Spark plans to integrate with Element Finance and Sense Finance to offer fixed-rate borrowing and more diversified yield strategies.

In the initial phase of the Endgame plan, Maker will launch six MetaDAOs, each of which will issue Sub Tokens. Although Spark Protocol does not explicitly introduce its tokenomics in the documentation, according to the plan and description by Spark’s founder, the protocol should have its own token.

At the same time, each Sub Token will form a core liquidity pool with $MKR. The Maker team plans to incentivize LPs by issuing 45,000 MKR to the pool annually. This means that during the Endgame period, each MetaDAO will accumulate 7,500 MKR. Of course, liquidity pools related to ETHD, DAI, and MKR will also receive a small token reward.

Figure 7: Spark Roadmap

As the first application in the Endgame plan: Spark is expected to bring Maker over $10 million in annual revenue growth, while also marking the first time that the $MKR token has a liquidity mining scenario. We will further analyze this in the following sections.

Industry Trend: The Matrix-ization of DeFi Applications

The Spark Protocol’s lending platform will directly compete with established lending protocols such as Aave and Compound. Although Aave and Compound have integrated with D3M❾in the past, Maker’s limited D3M resources❿ in the future will inevitably be prioritized for Spark. This is because Ethereum’s mainstream DeFi protocols seem to have started a “matrix” competition.

Various DeFi applications are developing more native nested products based on the advantages of user assets or liquidity, leading to a trend of “matrixing”. For example:

Curve, originally a DEX, has been actively promoting its “stablecoin” $3CRV, trying to tilt as much incentive as possible to the $3CRV currency pair rather than individual stablecoin pairs. It has also announced a new overcollateralized stablecoin crvUSD in the middle of last year;

Aave, the leading lending protocol in TVL, also announced plans to launch its over collateral stablecoin $GHO last summer;

And FRAX, which has always shown flexibility in its thinking, launched Frax Lend in September last year, allowing users to borrow/mint FRAX from the official contract by paying the market rate instead of via the conventional minting mechanism, which is similar to MakerDAO’s D3M mechanism.

Among these protocols, MakerDAO has long held the top spot in terms of TVL. As of February 25, 2023, its collateral vaults hold $8.2 billion worth of collateral, which theoretically can be released as new lending funds. If achieved, MakerDAO could surpass Aave as the market’s largest lending protocol, and its strategy of entering the DeFi matrix could open up new possibilities for its ecosystem expansion.

Currently, GHO and crvUSD have not officially launched yet. However, we believe that compared to the difficulty Aave/Curve face in growing their GHO/crvUSD stablecoins, Maker’s difficulty in growing its lending business is much smaller. This is because:

For a new stablecoin, selling pressure is certain (primary minters can only choose between pledging or selling), while buying pressure is uncertain and highly dependent on whether Aave/Curve can create enough use cases within their own & partner ecosystems. Looking at the performance of the second-ranked decentralized stablecoin Frax, which has been around for two years, its market capitalization is almost less than a quarter of DAI’s, despite controlling a significant portion of voting power in the ‘Curve War’. This shows that even with subsidies that help create usage scenarios, it is evident that there is a ceiling for Frax’s expansion.

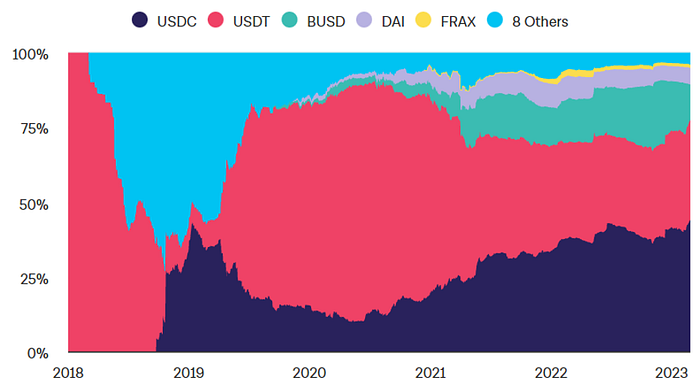

Figure 8:Stablecoin Market Share on Ethereum

Stablecoin governance is difficult and requires governance representatives with high levels of expertise to participate in its maintenance. MakerDAO is one of the earliest (founded in 2015) and most mature DAOs for governance, attracting a group of professional DeFi and monetary banking researchers who have led DAI through several leveraged and deleveraged spirals, effectively accumulating stablecoin governance experience. It must be acknowledged that Aave/Curve’s governance forums are also very active, but unlike lending, governance failure for stablecoins can easily lead to a “death spiral” that can cause the protocol to collapse. In this respect, Aave/Curve still has a long way to go.

The threshold for establishing liquidity is high, and the window of opportunity is limited. For a new stablecoin to be adopted by users, in addition to high rewards for staking in certain locations, it is even more important to have good depth and low slippage when performing its primary function as a “trading medium”. This means that the issuer of a new stablecoin may need to heavily subsidize and incentivize users to deposit their stablecoins for liquidity to other tokens in the early stages and cultivate enough user stickiness before subsidies decline to a point where they lose their attractiveness. Otherwise, LPs will begin to withdraw, transaction experience will decline, and de-pegging will occur frequently, marking the moment when the stablecoin enters the death spiral.

MKR Use Case Transformation: Staking+Liquidity Mining + Doubling of Burning Quantity

The launch of Spark represents not only a product update, but also the beginning of a major transformation of the Maker ecosystem. Most evident is the marginal improvement of the $MKR, and the valuation system will need to evolve from a single-project token to an ecosystem token similar to that of public chains. This is because the $MKR token, which previously only had governance rights, will now have single token staking + liquidity mining scenarios that we estimate staking $MKR alone may get an APY of 12–37%. At the same time, the expansion of ecosystem applications will effectively expand Maker’s balance sheet, bringing in an additional $10–20 million in annual revenue for Maker under the baseline scenario, which will result in a 1–3 times increase in the amount of $MKR burned.

General collateral lending has opened up asset inter-borrowing types, increasing protocol revenue streams.

As a leading DeFi protocol, MakerDAO has significant network effects, and Spark’s potential TVL is expected to be on par with Aave. Among the various asset types in the Aave ecosystem, ETH and stablecoins gold have the largest market share. As an example, Aave V2’s market size reached $5.44 billion, with an annual revenue of $16.3 million. The market size of the top five assets, including USDC, DAI, ETH, WBTC, and stETH, is about $1 billion, accounting for one-fifth of its total market.

The collateral value locked in the MakerDAO protocol is now worth $8.2 billion, and the value of single-currency assets (excluding LP tokens and RWA assets) is $6.6 billion. The total supply of DAI is 5.2 billion, of which 4 billion is generated by pledging USDC. Based on this number, even releasing only 1/4 of the USDC from PSM can achieve Aave’s current TVL.

Figure 9:Distribution of Collateral Types in MakerDAO Vault

Using Aave protocol’s annual revenue as a reference, we can project Spark protocol’s revenue performance under different scenarios where 20%/35%/60% of MakerDAO’s existing liquidity (with a non-LP token and non-RWA asset size of $6.6 billion) migrates to Spark as a result of liquidity mining incentives. The projected revenue performance is as follows:

The Spark official team also assumed three scenarios: base, bear, and bull, for the protocol’s revenue performance. Readers can compare and refer to it. In the Bull Case, the expected revenue is higher than ours, which means that they have an optimistic estimate and may have 5 billion+ TVL. However, we believe that the expectations for neutral and pessimistic scenarios are relatively reasonable.

2.MakerDAO will transform from the current dual-token (MKR/DAI) model to a multi-token model, with MKR opening up liquidity mining scenarios.

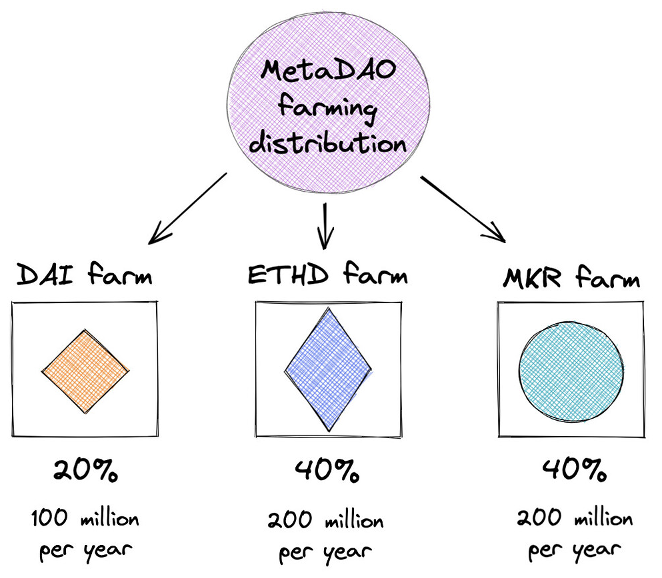

It is expected that when the new MetaDAO is launched, 2.6 billion MetaDAO (MDAO) tokens will be deployed, of which 2 billion will be released through liquidity mining, with 1 billion released in the first two years and then halved every two years. 400 million will be allocated to MetaDAO contributors and 200 million to the MetaDAO Treasury.

Figure 10:Distribution of Liquidity Mining Rewards

The liquidity mining allocation plan is as follows: 20% is used to incentivize the demand for DAI, 40% is allocated to ETHD Vault holders, and 40% is allocated to $MKR stakers.

For $MKR, staking represents a significant change in its economic model, as the supply and demand relationship of $MKR will thus be re-adjusted. Prior to this, $MKR had limited capture of protocol value as a governance token, resulting in insufficient market demand. In addition, in the event of debt shortfall, there is a possibility of inflation⓫ due to the need to increase the issuance of tokens to make up for it.

Although protocol surplus can repurchase and burn $MKR to make it deflationary, it seems to be insignificant. In the five years since $MKR was launched, only 22,000 tokens have been burned out of a total of 1 million tokens, resulting in an average annual deflation rate of 0.4%.

Figure 11:MKR Issuance and Burn History

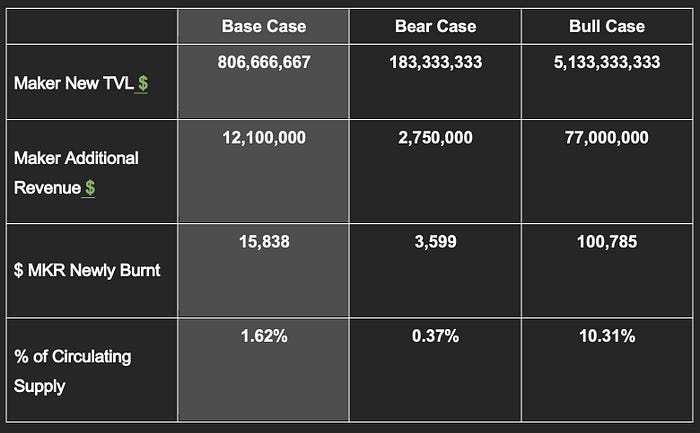

Because the expansion of Spark’s lending business will bring additional TVL and generate additional fee income for MakerDAO, Spark has also provided simulated income as a reference for MakerDAO.

If we calculate the expected Maker new TVL and MKR annual deflation rate based on the average stability fee of 1.5% and the current MKR price of $764⓬ under the three scenarios, the base-case scenario may bring Maker an additional TVL of $800 million, annual revenue of $12 million, and an annual deflation rate of 1.6%, which is four times the current rate. However, in the bear-case scenario, it may only bring less than $200 million TVL growth and $2.75 million annual revenue, but even so, this will correspond to an annual 0.37% MKR burn rate.

The above is based on the assumption of linear burning. In reality, MakerDAO will trigger the buyback mechanism only when protocol surplus reaches $250 million. Current surplus is only $74 million, which has not yet reached the buyback and burn standard⓭.

With the improvement of Maker’s revenue structure, the burning rate of $MKR should accelerate. At the same time, the opening of staking is expected to significantly improve the supply and demand relationship of circulating $MKR and will consequently be reflected in the price performance.

3. MakerDAO is shifting its focus from being a standalone protocol to building a DeFi ecosystem around stablecoins.

The goal of stablecoins is to expand their acceptance and usage as much as possible. MakerDAO has been working to collaborate with top DeFi protocols such as Aave and Compound. With the establishment of the MetaDAO model, Maker will build its own DeFi ecosystem around stablecoins as the core, and recycle the value of stablecoins back into the Maker ecosystem to enhance the overall valuation of $MKR.

Using the current price of $764 for $MKR and Spark tokens staked for mining as an example, simulations and predictions were made assuming that the value of Spark tokens could reach 35%/20%/60% of the value of Aave tokens in base, bear, and bull scenarios. The expected APR for 20% of $MKR participating in staking ranges from 12% to 37%.

It should be noted that this is a very preliminary and static assumption. Clarity on actual APR will have to wait as more details on Spark tokenomics are yet to be released. APR will also depend on the change in the price of $MKR.

4. MKR Expenditure Slowing Down

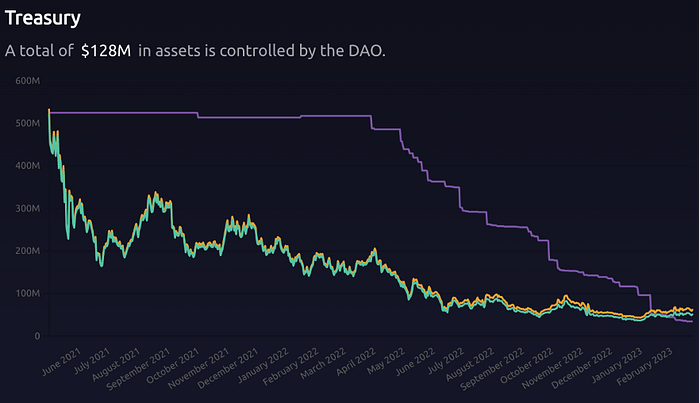

By outsourcing financial functions to new teams, MKR expenditures in the treasury will also slow down. As a result, the token supply-demand relationship will enter a natural state of market equilibrium. For example, from February 2022 to now, the treasury has spent nearly 13,000 MKR, bringing millions of dollars in selling pressure to the market.

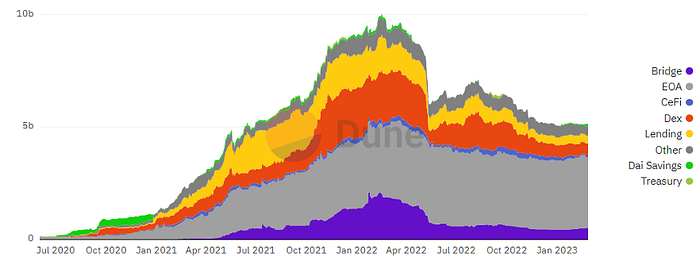

Figure 12:Treasury

Conclusion

The essence of the Spark Lend, the first application of the ‘Endgame Plan’, is to bring the capital-efficient D3M module, which was previously limited authorized for use by very few third parties, in-house. This eliminates security and governance risks that external protocols may cause, and the addition of the PSM module allows $DAI to maintain its cost advantage in the stablecoin war. Compared to variable rate competitors such as Aave or Compound, $DAI also offers more certainty in the interest rates charged, and users do not have to constantly check their borrowing costs.

Following Spark, there will be a series of subDAO projects whose tokens can be reward for $MKR staking. This greatly increases the revenue scenarios for $MKR while isolating risks. This marks the first time that $MKR has had an exogenous source of income through the staking mining scenario. In addition, Maker’s ecosystem may further incentivize trading liquidity LP for subDAO tokens with $MKR/$DAI, potentially changing the valuation framework of the token from a single project token to a token similar to Layer 1 ecosystems.

$DAI, as the most successful decentralized USD-pegged stablecoin, has been widely used in various DeFi applications, whether it is borrowing, trading, liquidity mining or other applications. However, the disadvantage is that the increase in the usage of $DAI seems to have not contributed enough to the sustainability of the Maker ecosystem. The project has entered a state where the bigger it gets, the more it loses. In addition to the technical and market operations required to maintain this complex system, high-quality governance talents and proposals must also be incentivized to make Maker sustainable. Given that the main incentive method is only through stablity fee revenue and $MKR tokens, the essence of the Endgame series product upgrade can be understood as:

- Breaking down the original silos of collateral within Maker and allowing for inter-collateral borrowing which would enhance capital efficiency, increase revenue streams for the project..

- Capturing the value of the $DAI use cases outside the Maker ecosystem into the internal ecosystem, similar to a bank’s diversified business expansion, providing end-to-end services to meet customer needs.

As a result, it is expected to achieve a simultaneous increase in the asset lock-in volume within the Maker ecosystem, DAI minting volume, and $MKR price.

Appendix

Risk Warning

The conservative setting of the D3M low-interest minting hard cap significantly limits Spark’s ability to help Maker “expand its balance sheet” and has some constraints on the overall size of assets in the Maker ecosystem..(Of course, the debt ceiling of D3M is not the higher the better. It should be considered in conjunction with the market demand for $DAI and price stability.)

Maker has invested more than 700 million RWA assets and plans further exposure, but there are regulatory risks: 1) there is a potential risk of freezing the RWA collateral itself; 2) the risk of partner institutions going bankrupt, such as Centrifuge, which has met a 6 million loan defualt; and the planned asset manager for Maker, Coinshares, has admitted that if there are regulatory questions, it will have to cooperate with regulatory scrutiny of fund sources, which means that temporary freezes/seizures may occur.

The marketing ability of the Spark project is still unknown: first, founder Sam MacPherson holds multiple positions and is currently the CTO and co-founder of game company Bellwood Studios. It is crucial whether he has sufficient energy and time to devote to the future development of Spark. Second, the Spark Operations Director is @nad8802, the current Chief Growth Officer of MakerDAO. Based on past performance, his approach to marketing may be relatively laid-back.

There is a possibility that DAI may abandon its anchoring with USD, resulting in a large number of users leaving in the short term. Although this may be beneficial for $DAI to become the ultimate decentralized currency with stable purchasing power (rather than via the USD exchange rate), the community has not reached a consensus, and it is only the unilateral idea of founder Rune, which is planned to be the focus of discussion around 2025. Vitalik Buterin has expressed his concerns about this.

There is a risk of changes to the $MKR feedback mechanism. Currently, there are discussions in the governance forum about how protocol revenue can repurchase MKR or even reduce repurchase, and the reward of subDAO tokens to MKR in Endgame may also change as governance discussions deepen. Overall, the core members of the Maker community are relatively conservative and not eager for quick money.

Decentralization under regulation may conflict with the true spirit of decentralization. The reason is that Oasis, the front-end provider for MakerDAO, recently helped a third-party authorized by the court, Jump Crypto, to recover 120,000 ETH stolen by attackers from the cross-chain bridge Wormhole in February last year. Because the attacker deposited the funds in Oasis, Jump Crypto used the upgradable agent mode in the Oasis protocol to change the contract logic automatically, transferring the collateral and debt from the attacker’s treasury. Although Oasis made this decision under legal intervention and the MakerDAO protocol itself does not control any front-end provider or product that allows end-users to access Maker Vault, it ultimately violates Maker’s mission to make DAI a fair world currency. Of course, this also demonstrates the necessity and importance of Rune’s early planning of regulatory defense strategies.

Potential security risks in smart contracts. Even after strict audits, no code can be said to be 100% secure, and its maturity and reliability need to be tested by the market. Users must remain vigilant against this kind of risk.

The Basic Mechanism of MakerDAO

MakerDAO is a decentralized stablecoin lending protocol based on Ethereum, which is backed by over-collateralized assets and lends out stablecoin DAI that is pegged to the US dollar at a 1:1 ratio. By adjusting the stability fee through governance, the market can stabilize the price of DAI through arbitrage. When the value of collateralized assets is insufficient, the system forces the sale of collateral to liquidators to ensure debt repayment.

Overview of Maker System Data

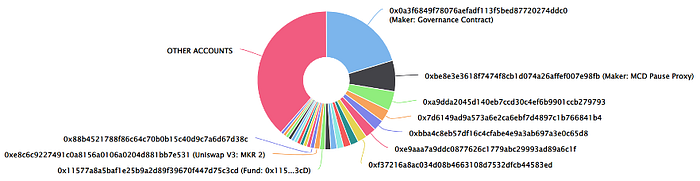

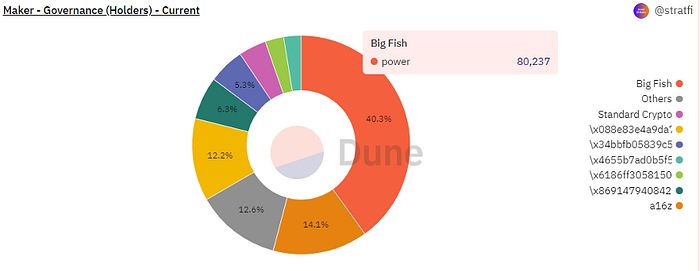

Top 25 Holder Addresses: Token distribution is relatively diversified

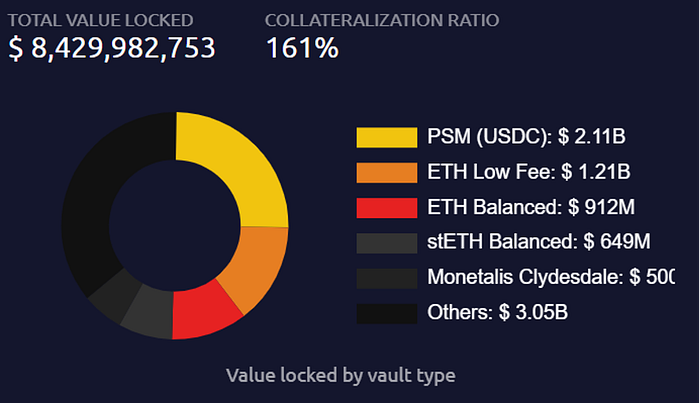

MakerDAO Vault Collateral Value & Types

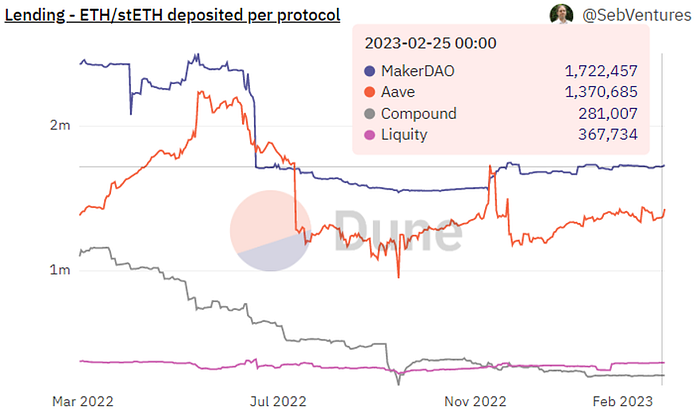

Changes in the distribution of ETH/stETH within mainstream lending protocols: MakerDAO has the largest share.

Annual revenue overview of MakerDAO protocol.

RWA debt distribution: the largest debt is generated by Monetalis Clydesdale.

DEX Distribution of DAI: The largest proportion is held in EOA accounts, followed by DEX.

Distribution of MKR governance weight.

Historical Events and Milestones of MakerDAO:

In 2013, Daniel Laimer, the founder of EOS, proposed the concept of a Decentralized Autonomous Corporation (DAC), which was one of the precursor concepts of DAO.

In March 2015, Rune Christensen founded MakerDAO and began planning a stablecoin pegged to the US dollar.

In December 2017, MakerDAO released the first version of the DAI stablecoin and launched the first version of its smart contract on the Ethereum network.

In 2018, MakerDAO made its first adjustment to the DAI stability fee, lowering the borrowing interest rate from 1.5% to 0.5%.

In September 2018, venture capital firm Andreessen Horowitz invested $15 million in MakerDAO by purchasing 6% of the total $MKR token supply.

In February 2019, MakerDAO launched the Multi-Collateral DAI (MCD) system, which allowed users to generate DAI using various types of collateral.

In November 2019, Maker released MCD, which supported borrowing DAI with multiple types of collateral assets.

In January 2020, the total supply of DAI surpassed 100 million.

In March 2020, a market crash caused Ethereum prices to plummet, resulting in a debt shortfall of $5.3 million, which was covered by auctioning off MKR tokens.

In April 2020, the Maker Foundation announced that it would transfer control of the MakerDAO protocol to a decentralized community governance system.

In May 2020, MakerDAO launched a decentralized governance system based on on-chain voting.

In November 2020, the total supply of DAI surpassed 1 billion.

In 2021, MakerDAO introduced the D3M mechanism, which provided a more flexible and low-cost way for collaborating lending platforms to mint DAI.

In April 2021, Maker’s Liquidation Mechanism 2.0 went live, and the Wyoming state legislature officially approved the DAO bill, allowing DAOs to be registered as limited liability companies in the state.

In May 2021, the Maker Foundation returned the 84,000 MKR assets held by the Dev Fund to the DAO.

In February 2022, the supply of DAI exceeded 10 billion for the first time, and Maker announced a multi-chain deployment plan.

In August 2022, MakerDAO partnered with Huntingdon Valley Bank (HVB) of Philadelphia to link its native stablecoin DAI with regulated US financial institutions for the first time.

In October 2022, Maker proposed a community initiative to invest 1.6 billion USDC in Coinbase Prime for investment purposes.

In December 2022, MakerDAO announced a $220 million real-world asset fund in partnership with BlockTower Credit, with MakerDAO deploying four vaults providing a total of $150 million in the capital.

In February 2023, MakerDAO announced the creation of the Spark Protocol, a universal lending protocol.

Reference materials

《endgame-docs-staging》

https://makerdao-1.gitbook.io/endgame-docs-staging/tokenomics/subdao-tokenomics

《MIP116:D3M to Spark Lend》

https://forum.makerdao.com/t/mip116-d3m-to-spark-lend/19732

《Announcing Phoenix Labs and Spark Protocol》

https://forum.makerdao.com/t/announcing-phoenix-labs-and-spark-protocol/19731

《MakerDAO Valuation》

https://messari.io/report/makerdao-valuation

《Endgame Communications Strategy & Plan》

https://forum.makerdao.com/t/endgame-communications-strategy-plan-community-feedback/19818/2

《Endgame Plan v3 complete overview》

https://forum.makerdao.com/t/endgame-plan-v3-complete-overview/17427

《MakerDAO Governance Risk Framework》

https://blog.makerdao.com/makerdao-governance-risk-framework/

Footnote

❶The team, formerly known as Crimson Creator Cluster, consists of four core members. Founder Sam MacPherson (@Hexonaut on Twitter) joined MakerDAO in 2017 as a core engineer and is also the CTO and co-founder of game company Bellwood Studios.

❷D3M, the Dai Direct Deposit Module, was first introduced in November 2021.

❸According to PhoenixLabs’ description in February, the rate is “slightly above” 10%, which means if the DSR is 1%, the user’s borrowing rate would be 1.1%.

❹According to the founder of PhoenixLabs on Twitter, there was no pre-allocation, but there may be uncertainty here due to the Endgame discussion draft for the subDAO project, which reserves 400 million tokens (out of a total supply of 2.6 billion) for incentivizing subDAO employees.

❺When the D3M module was launched, its purpose was to allow Maker to execute the maximum variable borrowing rate on the DAI market of its partner lending protocols, such as Aave. It does so by calculating how much DAI supply is needed to bring the interest rate down to the desired level and then minting DAI against the returned aDAI from Aave.

D3M has a specific target borrowing rate, such as 4%. Whenever the variable borrowing rate of DAI in the lending market exceeds 4%, anyone can call the exec() function of the treasury to readjust the amount of DAI in the pool. In this case, it will calculate the amount of DAI that needs to be minted to achieve the target rate and put it into Aave’s lending pool. This will continue to increase DAI until it reaches the debt ceiling or reaches the target of 4%.

On the contrary, when the variable borrowing rate falls below 4% and users have previously added liquidity, the exec() function will calculate how much liquidity needs to be removed to bring the target rate back to 4%. It will continue to remove liquidity until all the debt in the treasury is paid off or the liquidity in the pool is exhausted.

❻PSM allows users to exchange whitelist stablecoins (USDC, USDP, GUSD) for DAI at a fixed exchange rate (may including a 0.1% fee) of 1:1. Its main purpose is to help maintain the peg between DAI and the US dollar.

❼Assuming that Maker and Aave both have a 150% collateralization ratio.

❽In the community, later it was renamed as subDAO, which directly reflects the meaning of “subordinate DAO”.

❾The D3M collaboration module of Aave was launched in April 2021 with an initial credit limit of 10 million DAI, which was gradually increased to a limit of 300 million DAI. However, due to the volatility of the cryptocurrency market, it was temporarily closed in June 2022. The Compound V2 D3M module began operating in December 2022, with a current credit limit of only 20 million USD as of the time of writing.

❿Because the D3M system bypasses Maker’s Stability Fee system and uses the relatively lower DSR interest rate as its cost, rapid increase in the issuance of Dai may lead to oversupply, which could in turn cause the price of Dai to depeg. Therefore, in theory, the early D3M limit should not be raised too quickly, and further observation of its impact on the stability of the Dai price is needed.

⓫In the 2020 March 12 liquidation event, the Maker protocol incurred a deficit of 5.3 million USD and compensated for it by issuing 20,980 MKR.

⓬Data is sourced from Coingecko as of February 27, 2023.

⓭Due to increased market uncertainty, Maker suspended MKR buybacks and burns in the second quarter of 2022, sending all protocol revenue to the DAI buffer. Normally, Maker would use DAI to buy MKR directly from the MKR-DAI liquidity pool of Uni V2 and then burn it. However, the community is also discussing using the repurchased MKR for new holding incentive plans, or investing the repurchased MKR instead of fully burning it.