by Chris Powers

Protocol governance rushes to stem losses from users’ high-levered stablecoin bets.

It seems like every few months, there’s a black swan event in crypto. In just the last three years, there’s been Black Thursday at the start of Covid, DeFi summer 2020, the 2021 bull market, Luna/3AC, and then the FTX collapse. The failure of SVB and the burgeoning banking crisis that’s unfolded over the last two weeks is the latest unprecedented incident.

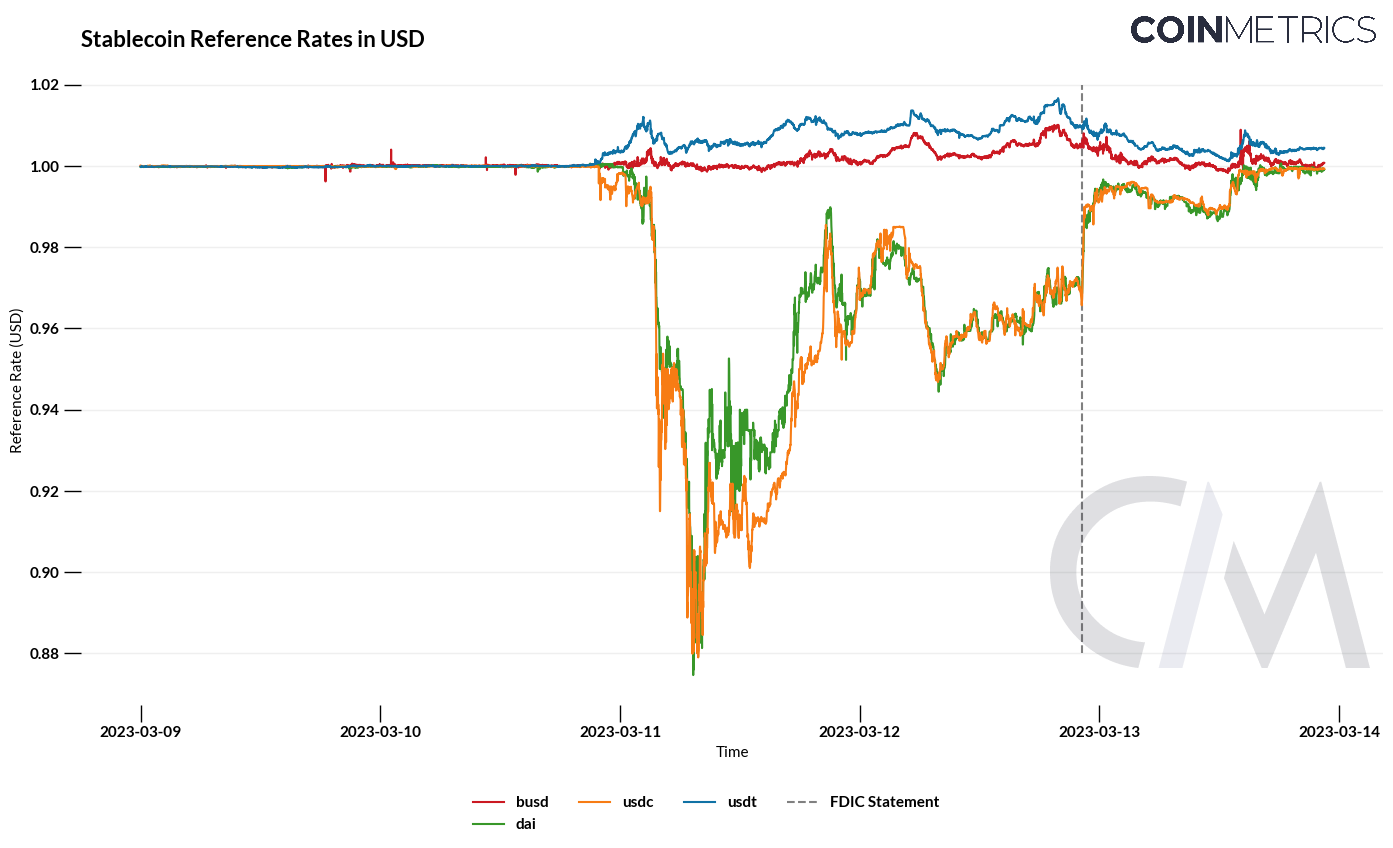

Soon after the FDIC announced it had taken over SVB on Friday March 11, USDC – the most trusted stablecoin – began drifting from its peg. It then plunged when Circle revealed it had $3.3bn of cash locked up at SVB, and then dropped further when they halted redemptions before bottoming out at $0.87. As the weekend went on and with markets closed, USDC’s on-chain price became a proxy recovery rate for SVB depositors, trading sideways below its $1.00 peg. This carried on until the FDIC announced on Sunday evening that all SVB deposits would be accessible at Monday’s market open.

As the chart above from Coin Metrics shows, USDC wasn’t the only stablecoin on the move. Dai (aka “wrapped USDC”) mirrored USDC’s price, while USDT traded at $1.01+, as investors were willing to pay a premium for stability.

DEX volume soared on-chain, posting an all-time daily high of $25bn (Uniswap ended at $12bn, while Curve had $8bn). MEV-Boost also posted an all-time high. For a DEX, a depeg – or any volatility – is a good thing; there’s no strain on the system and fees skyrocket. This is not true for DeFi lending, where a depeg could destroy a protocol if risk and volatility are not properly governed.

Lending in volatility

Each of the major lending protocols (Maker, Aave, and Compound) responded quickly with emergency governance actions, and are now discussing long-term changes to insulate their protocols from failure in the event of another depeg. The impact of these changes will hinge on whether they heed the key lessons from this latest incident (more on that later). First, here’s how the Big Three fared:

Maker

- Where they were: Prior to the USDC depegging, Maker held $2.4bn of USDC (5% of USDC’s circulating supply). Almost all of this sits in Maker’s Peg Stability Module (PSM), which enables 1:1 exchange between Dai and USDC.

- During the depeg: As investors sold USDC (typically for USDT) and pushed down the price, many USDC holders deposited their USDC in the PSM, minted Dai, and then sold the Dai. This meant that Dai’s price slightly lagged USDC’s price, because the PSM enabled the same sell pressure on Dai by allowing 1:1 minting. This resulted in $2bn of additional USDC inflows, which Maker is now stuck with. MakerDAO governance went into emergency mode, adding a 1% fee to the PSM (plugging the hole), reducing the debt limits on all USDC-based collateral, and increasing the debt limit on USDP (which didn’t suffer depegging issues). It also updated protocol parameters to allow debt ceiling adjustments to bypass the Governance Service Module (GSM) Delay.

- Going forward: Dai is now more backed by USDC than it was prior to the depeg. No one in the Maker community is particularly happy about this, but in typical DAO fashion, they still can’t agree on a plan to wean themselves off of USDC. Increasingly, it looks like Maker will follow in the direction of its founder, Rune Christensen. He also prefers the most extreme option: decoupling Dai from the US dollar to become an independent stable currency. It’s hard to square this vision with the reality of the here and now. There’s almost $6bn of Dai in circulation that desperately wants to be pegged to the dollar. Rune’s ideas don’t seem to acknowledge that Dai is a product that already has market adoption. And right now, it still needs to operate within the confines of its self-imposed USDC straightjacket.

Compound

- Where they were: Compound is in the midst of transitioning to v3, while also trying to go multi-chain and claw back some market share from Aave. USDC was hardcoded at $1.00 in its v2 contracts, and Compound exclusively uses it as the borrowing asset in v3.

- During the depeg: The Compound v2 Pause Guardian (a multisig) halted USDC supply transactions, while continuing to allow all borrowing. It did not pause Dai supply transactions even though it mirrored USDC’s fall, likely because the protocol adapted to its price decline because it was not hardcoded. Notably, Gauntlet recommended pausing borrowing for all assets, a much more aggressive step that was not implemented. Their concern focused on Compound users who were recursively borrowing – simultaneously supplying a stablecoin while also borrowing a stablecoin. Given the high loan-to-value ratio (LTV) of stablecoins and their price correlations, traders are able to make a levered bet while also farming COMP. The biggest risk of this activity during the depeg came from an address that supplied 20.7m USDC and borrowed 17.1m USDT.Presumably, this was a leveraged bet to short USDT. That was not the correct bet following the USDC depegging, but with the price hardcoded at $1.00, this position was safe.

- Going forward: All eyes are on v3 and Compound’s expansion to other chains, with Arbitrum and Optimism up first. Compound did not take any risk mitigation measures on v3 during the depegging event, because “Compound v3 features an upgraded risk engine”. On v3, only USDC is borrowable, so there was no risk of bad debt accruing because USDC is not used as collateral.

Aave

- Where they were: Aave has always been the most aggressive lending player, whether it be via marketing, adding new assets, or expanding to new chains. It released its v3 six months before Compound, and was further along in the deployment process; v3 was running live on Avalanche, Arbitrum, Optimism, Polygon, and Mainnet. While not yet implemented on all chains, v3 also features E-Mode (efficiency mode), which enables higher borrowing power for assets with correlated prices.

- During the depeg: USDC was not hardcoded to $1.00, so the protocol’s oracle instantly registered the declining price of the more-than 1 billion USDC deposited into Aave. On v2, with a LTV ratio of 85%, the protocol would only take on losses if USDC dipped under $0.85 and failed to stabilize. So while the Aave war room debated whether to pause v2 on Ethereum (the largest market), it ultimately did not and USDC’s peg eventually recovered. Outside of Ethereum, there were issues: Aave incurred bad debt and had to take emergency action. This was for two reasons. First, there was less USDC liquidity on smaller chains, with most of it bridged USDC (as opposed to native). Second, Aave v3 on these smaller chains had E-Mode enabled. This allows borrowing of up to 97% of stablecoin collateral and has a liquidation threshold at 97.5%, so there’s a very tight band for healthy liquidations.As the price of USDC dropped, many recursive stablecoin borrowers should have been liquidated (when USDC hit $0.97), but most were not – USDC liquidity was crumbling so it wasn’t appealing to liquidate (especially with a low liquidation penalty). As the price of USDC continued to drop, the protocol missed the window for healthy liquidations (where the value liquidated and returned to the protocol exceeds the outstanding debt that is paid off). Avalanche was hit worst worst, incurring almost $300k of bad debt. This prompted the Aave Guardian to freeze the USDC, USDT, Dai, Frax, and Mai markets on Aave v3 Avalanche.

- Going forward: The Avalanche markets were unfrozen earlier this week, with plans for the supply caps to be drastically reduced. And now, Aave governance is discussing what adjustments to make to E-Mode, which is leading to a frank discussion on what exactly is the target use case for E-Mode. The main problem during the depeg was that some of the assets in E-Mode depegged together (USDC/Dai) while others did not (USDT). E-Mode leaves a protocol susceptible to a depegging incident, which is by nature hard to predict. Aave has yet to pass any changes to E-Mode, but the current community consensus seems to be to reduce the LTV ratio for stablecoins in E-Mode to insulate the protocol against the risk of a depeg. Any adjustment to E-Mode parameters will lead to significant liquidations if positions are not unwound before the change is put into effect.

Three takeaways for DeFi lending

First, recursive borrowing may not be worth the heightened risk. Borrowing and supplying the same stablecoin is not risky to the protocol – although we do question its utility to the protocol; the bigger risk to protocol solvency is from users that simultaneously supply one stablecoin and borrow another. Recursive borrowing is profitable for the user because of protocol or chain rewards, and protocols like it because it can juice its revenue (E-Mode on Avalanche yielded almost $2.5m last year). Is the revenue and user growth enough to justify the added risk? A possible future influence on the answer may be the emergence of the ETH liquid staking derivatives (LSD), which will completely upend the lending market. Having a system (like E-Mode) that could efficiently manage multiple LSDs as collateral could be very appealing to borrowers.

Second, USDC may become more entrenched into lending protocols. It’s complex to manage multiple stablecoins in a shared lending pool. As more lending moves into isolated pools, those will likely come with a single borrowable asset (like Compound v3). You could have a ETH-USDC, ETH-Dai, ETH-USDT pool, but protocols may drift towards a preferred stablecoin as not to siphon liquidity. Aave’s E-Mode would have less insolvency risk if it only included USDC-backed stablecoins (like Dai and Frax).

Third, a governance system and community that can respond in real time is crucial to ensuring adequate risk management. DeFi OGs will recall the confusion and panic in Maker governance in the months following Black Thursday in 2020, when Dai consistently traded above its $1.00 peg. Those DeFi days are over. Unlike in 2020, there was a swift response and active discussion amongst a wide range of stakeholders at Maker, Compound, and Aave following the depeg. Some may think that DeFi must prioritize governance minimization, but for a lending protocol governance is an unavoidable reality, given the need to balance capital efficiency and protocol solvency.

It was not a flawless weekend for DeFi, but the quickness of the governance response underscores how far off-chain coordination in DeFi has come.

Special thanks to Nick Cannon, Luigy Lemon and Ross Galloway for inspiration and feedback on this post.