【KEY INSIGHT】

- CEX Token has shown significant variation in performance over the past year: Only a handful of CEX tokens like BMX, BGB, and MX have surged by over 100% in the last year. By contrast, BNB and OKB saw comparatively lower increases due to their high level of market capitals.

- The Buyback And Burning Mechanism Plays A Decisive Role In The Value Of CEX Tokens:

CEX tokens like MX and GT restore their scarcity and thus preserve value by strictly following their preset buyback and burning schedules with a high burning rate. Conversely, kucoin’s burning rate is comparatively modest, constraining its growth potential. - As Native Assets on BlockChains, CEX Tokens Have Better Application Prospects: Cex Tokens, among which BNB and OKB are stellar, have evolved into native assets built by exchanges on public blockchains, serving pivotal roles within their ecosystems and bolstering their utility and demand.

- BMX Appears Undervalued:

According to the spot market share of BitMart, the market capital of its CEX token seems to be much lower than those of other mainstream CEX tokens, likely indicating an undervalued price of BMX. - BitMart’s Upgrade Plans Will Further Empower BMX’s Growth:

BMX’s utility and value are expected to be enhanced via the exchange’s next steps, such as BMX upgrades, the launch of Web3 wallets, and Layer 2 solutions.

【ABSTRACT】

Over the past year, benefiting from the listing of BTC ETF on the U.S. stock markets and the fourth halving of BTC supply, the price of BTC has once surged over $73,000 to reach a historic high. This attracts global attention to the performance of the cryptocurrency market. As one of the hot topics in the industry, CEX tokens have also demonstrated a solid upward trend. This article focuses on seven significant CEX tokens: BNB, OKB, BGB, KCS, GT, MX, and BMX. According to CMC data, the average growth of the seven CEX tokens’ prices is approximately 98.35% annually, showing a robust performance overall.

There is a current debate in the market on whether CEX tokens are overvalued and whether they provide a viable avenue for investment. This article aims to offer readers a comprehensive analysis of the seven selected CEX tokens, evaluate their value and potential,

and examine indicators of the growth of price and market capitals, buyback mechanisms, functional rights, and the market performance of their issuers.

【COMPARISON OF CEX TOKEN DATA】

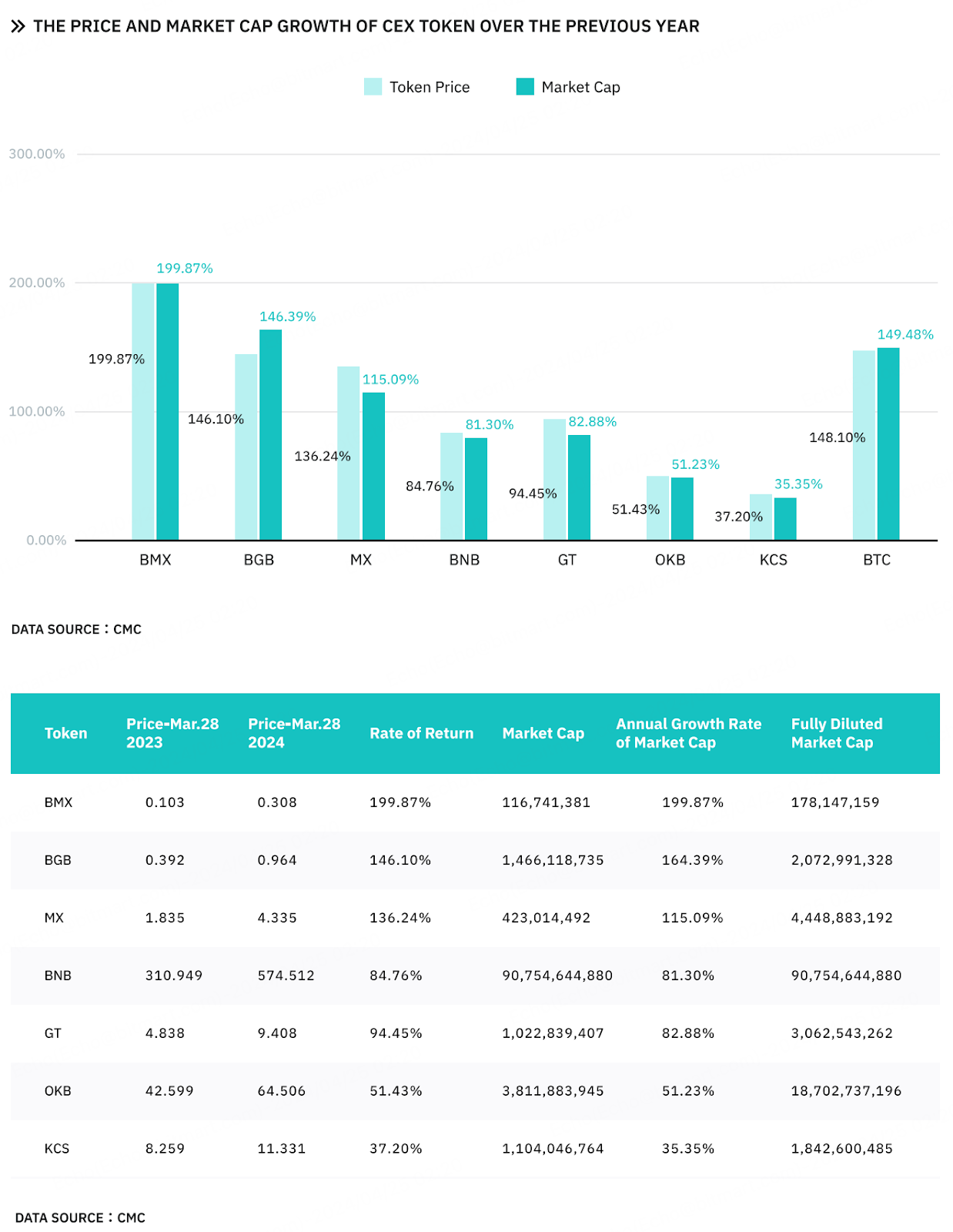

According to CMC data, the average annual price growth of the seven CEX tokens’ is approximately 98.35%, slightly lower than Bitcoin’s 148%. However, there are a few exceptions—BMX, BGB, and MX, which have seen price increases exceeding 100%.

While the price increases of BNB and OKB are relatively lower, 84.76% and 51.43%, respectively, it does not necessarily indicate poor performance. The figures may be attributed to their high market capitals. As one of the top CEX tokens, BNB’s market capital has reached 90 billion dollars, and that of OKB also approaches 4 billion dollars. Due to such high bases, the degrees of the two’s price fluctuations are more restricted, making it difficult for them to achieve as prominent growth as that of CEX tokens with smaller market capitals. Therefore, BNB and OKB, featured as two mature CEX tokens, have relatively limited growth potential as they have already occupied significant market shares. In contrast, CEX tokens with lower market capitals, such as BMX, BGB, and MX, have more significant growth potential due to lower market shares, presenting more growth opportunities.

It is worth noting that BMX has captured a remarkable price and market capital rise during the last year. Within the last year, BMX’s price staggered over approximately two folds of its initial value one year ago. Its market capital has surged over 249.79%. Those facts could, to some extent, reflect BMX’s strong market performance and recognition of its potential value.

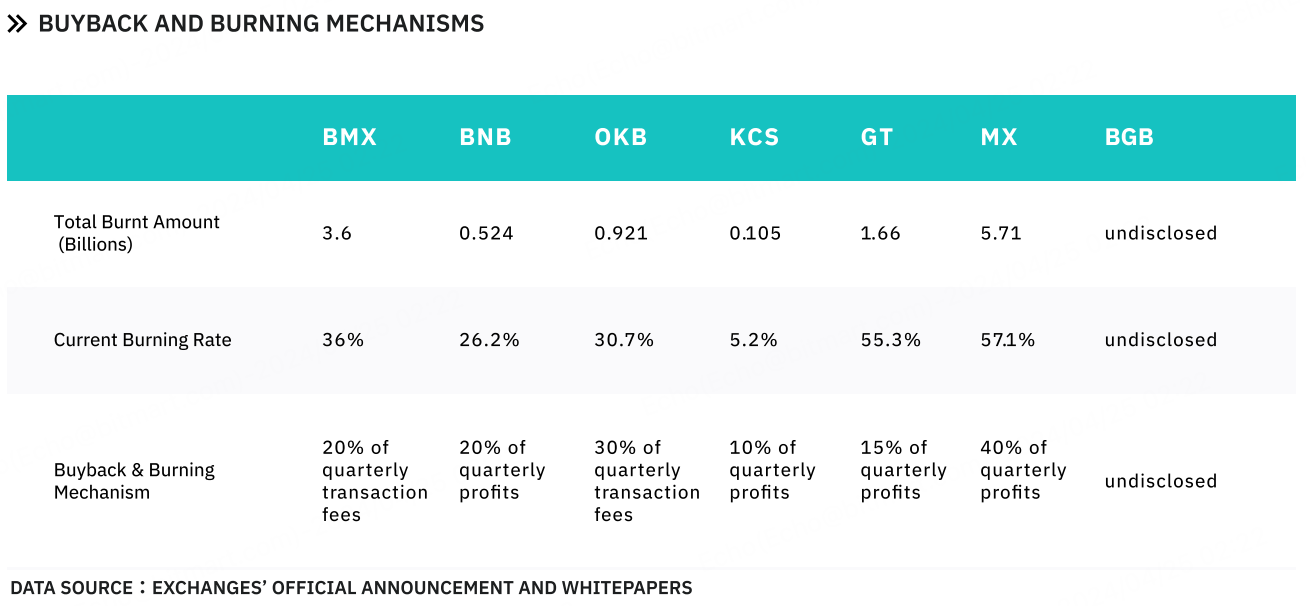

The buyback and burning mechanism is one of the primary ways to improve the value of CEX tokens. Exchanges reduce the circulating supply of their tokens by regularly buying back and burning them, thus achieving deflation and value increase. According to official announcements from those exchanges, MX and GT have the highest buyback and burn ratios, approximately 57.1% and 55.3%, respectively. Generally, the volume of tokens bought back and burnt varies between 10% and 40% of their profits. For instance, MEXC’s buyback accounts for 40% of its quarterly profits, while Kucoin’s is relatively lower, accounting for only 10%. This could possibly suggest that MEXC takes more proactive measures to reduce the circulated MX, thereby increasing its scarcity and value. By comparison, Kucoin’s buyback and burning rate appears much lower, which limits the appreciation of KCS. Therefore, although MEXC takes a smaller share on spot market than Kucoin, effective implementation of the buyback-and-burn mechanism has successfully hindered MX’s inflation, driving its market capital to 2.4 times of KCS.

Based on BMX’s whitepaper, BitMart’s quarterly buyback amount accounts for 20% obuf its transaction fees. Since the issuance of BMX, the burning rate has been approximately 36%. According to its burning plan, BitMart will continue to buy back BMX until its amount is decreased to 500 million (the total supply of BMX is 1 billion).

TOKENOMICS

Due to the long issuance history, some of the seven centralized exchange tokens’ detailed tokenomic information was not disclosed. Among them, BMX and BGB are the two that have officially published plans of token unlocks and distribution structure. It is believed that such detailed and unique token economic models can help promoting user engagement, enhance market liquidity, and increase asset values.

Data Source:BMX’s WHITEPAPERS

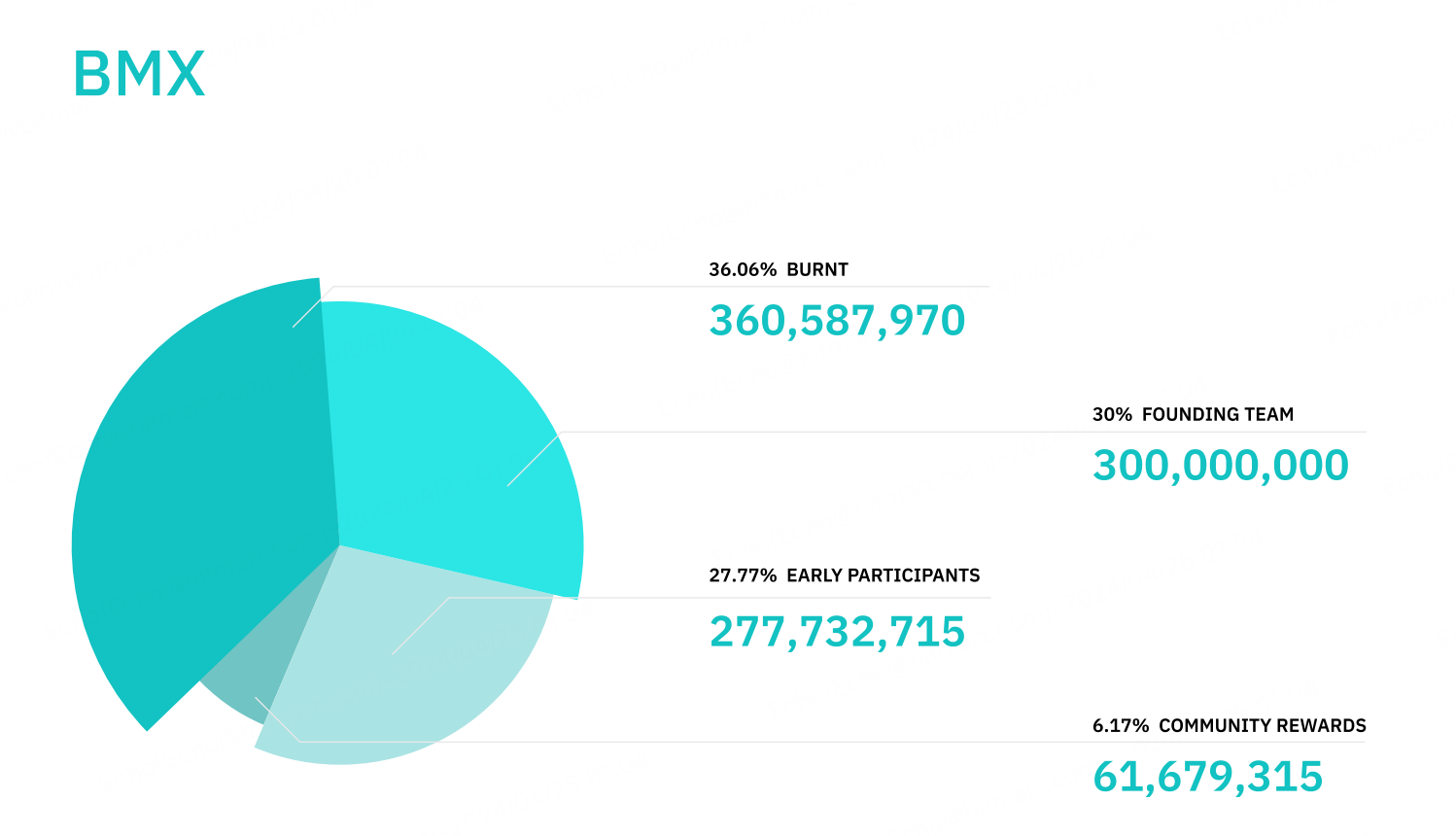

The total supply of BMX is 1,000,000,000. The tokenomics design a deflationary mechanism through token buyback and burning and a reward mechanism. As of April 26, 2024, the current circulating supply of BMX stands at 324,281,616.

· 36.06% will be repurchased and burned.

· 6.17% is allocated for community rewards.

·30% is allocated for team incentives, and 75% of BMX has been locked for three years. As of April 26, 2024, those portions remain locked (0x865acE374B47fCBFB41Ac458260a30ac4F3231C6).

·27.77% is allocated to early participant incentives.

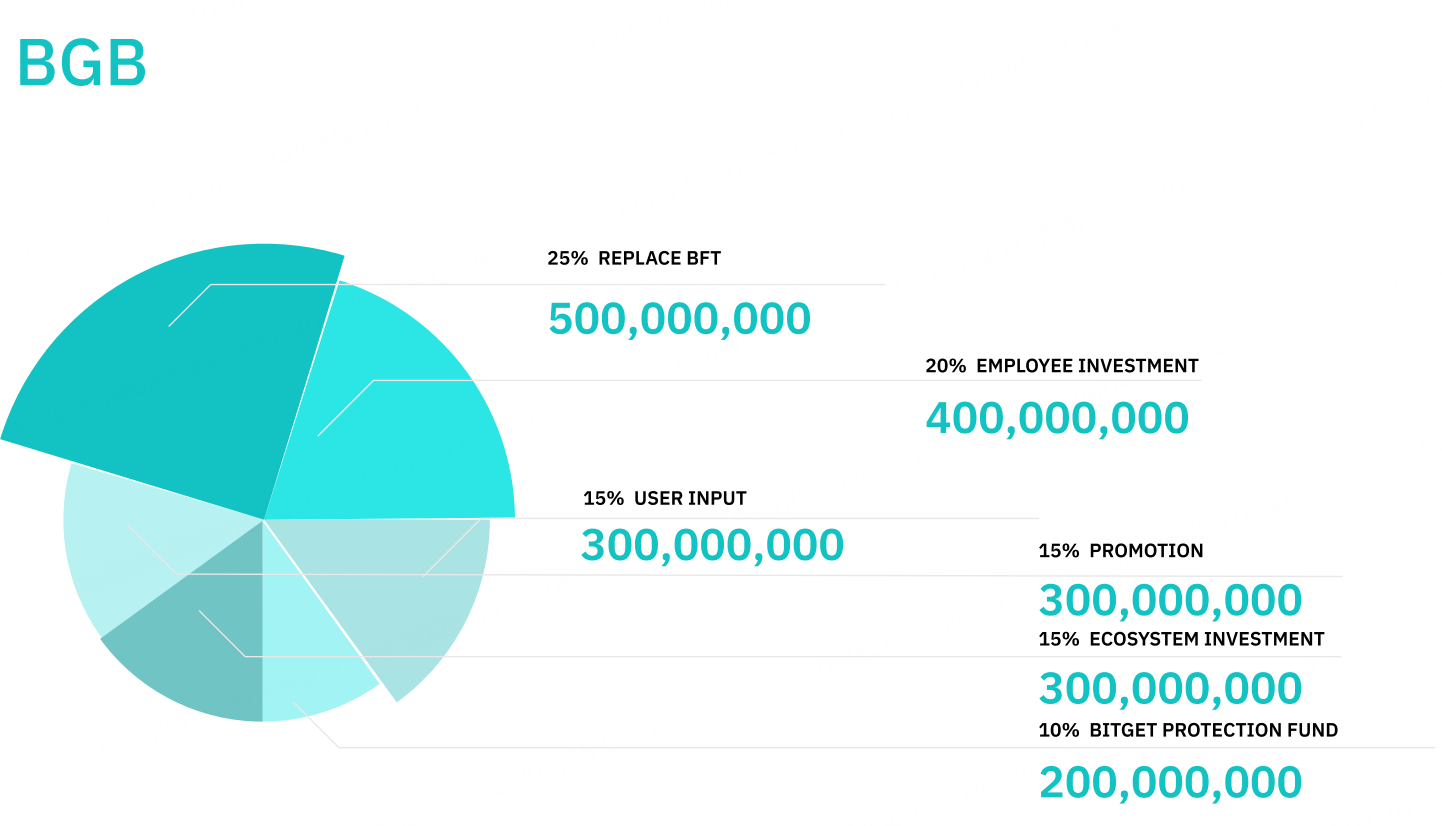

Data Source:Bitget’s OFFICIAL ANNOUNCEMENT

The total supply of BGB is 2,000,000,000, with 25% swapped for BFT holders. The remaining 75% will be distributed for community acquisition, branding and growth, ecological investment funds, core team motivation, and investor protection. Specific release schedules and conditions apply for each allocation. Currently Bitget does not disclose the burning and repurchase mechanism of BGB.

·25% Replace BFT, Used to swap out existing BFT tokens

·20% Employee investment, 2% unlocked every 6 months, fully unlocked within 5 years.

·15% User input, Releases up to 4% per year.

·15% Promotion, Releases up to 3% per year.

·15% Ecosystem investment, Released to the Bitget ecosystem investment fund.

·10% is allocated to early participant incentives.

【ANALYSIS OF TOKEN FUNCTIONALITY】

Currently, CEX tokens’ major application scenarios can be divided into the following three: Exclusive Rights, Trading Rights, and Native Assets for Blockchain Networks. Here are detailed explanations and examples of those categories:

Exclusive Rights:

On most exchanges, a register’s total position of CEX tokens is often a criteria of determining the account’s membership or user benefits level. Token holders enjoy prioritized customer services, exclusive event access, or special withdrawal privileges on that platform. Those benefits are often linked to the number and durations of tokens held on accounts. Exchanges utilize this function to enhance user loyalty and stimulate daily activities on platforms.

Trading Rights:

Compared to exclusive rights, trading rights are more directly connected to exchanges’ core business—trading. Platform token holders may enjoy discounts on trading fees, more favorable trading tiers, and prioritized access to new listed coins. Additionally, exchanges might open more access for token holders to products with higher risks – derivatives, for example, margin trading, futures and options. Those benefits are designed to boost trading volume and strengthen adhesiveness of users.

Native Asset Of The Blockchain:

In the case of exchanges developing their public blockchains such as Binance Smart Chain (BSC), OKChain, and KuCoin’s KuChain, tokens like BNB, OKB, KCS, and GT become the native assets in the corresponding protocols. They serve a dual purpose:

1) Universal Gas Resource: it is usually the sole payment mechanism of transaction fess on chain.

2) Network Governance: token stakeholders will be responsible for various governance decisions such as voting on protocol upgrades and policy adjustments.

The ongoing developments of those blockchains can help promoting the usability and demand for their native tokens as more developers and projects opt to build applications on them, and thus extends their usage scenarios.

With the above mentioned functionality, CEX tokens play critical roles in their dominated ecosystems. All those features expands their utility and theoretically raises their demands. As a result, the value of CEX tokens tend to closely tied to the development of their governed protocols.

【COMPARISONS OF CEXES’ MARKET PERFORMANCES】

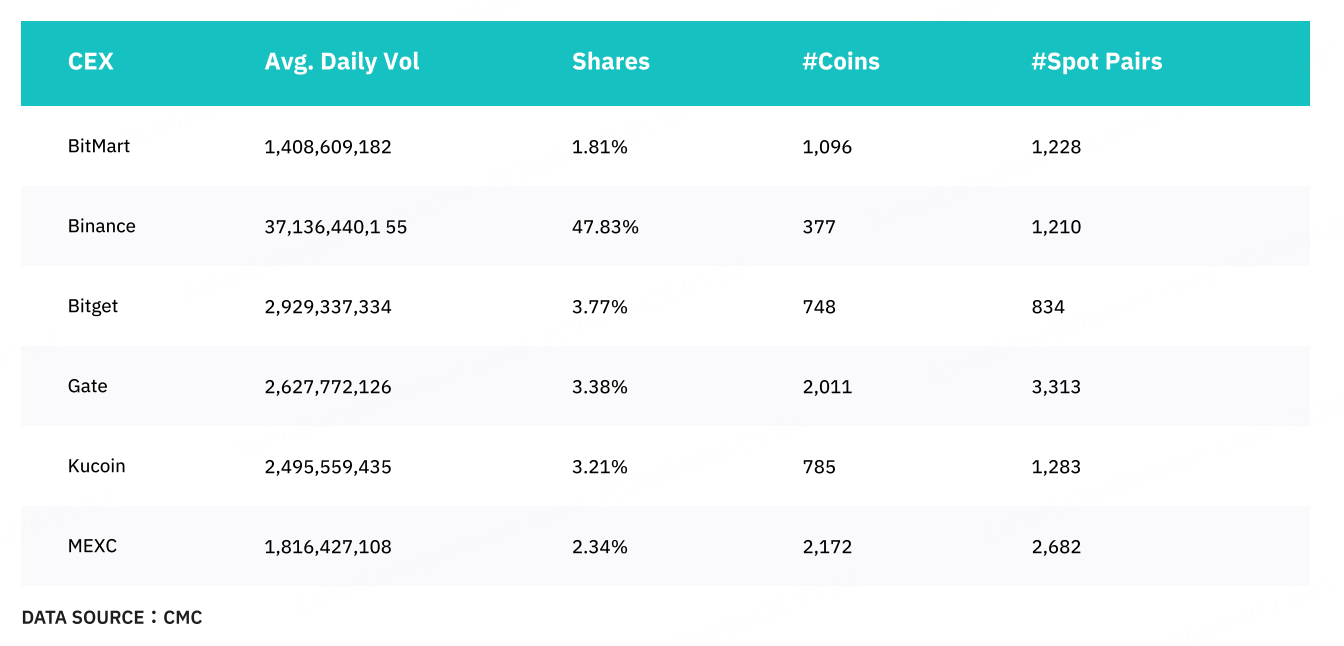

SPOT MARKET SHARE, SPOT TRADING VOLUME AND THE NUMBER OF SUPPORTED SPOT TRADING PAIRS

Trading Volume And Market Share:

According to CMC data, Binance leads the pack regarding market share (measured by trading volume), capturing most trading activities across the market. Except for Binance and OKX, the other exchanges present similar and relatively close market shares, roughly around 1.5% to 4%.

BitMart’s market share is around 1.81%, close to MEXC’s, and is considered a second-tier exchange.

Supported Spot Currencies And Spot Trading Pairs:

Regarding the number of supported spot currencies and spot trading pairs, Gate and MEXC are ranked in the top 2. Gate supports 2,011 spot currencies and 3,313 spot trading pairs, while MEXC supports 2,172 and 2,682, respectively. BitMart supports over 1,000 spot currencies and spot trading pairs, providing diverse trading options.

【EXPLORING THE POTENTIAL OF BMX】

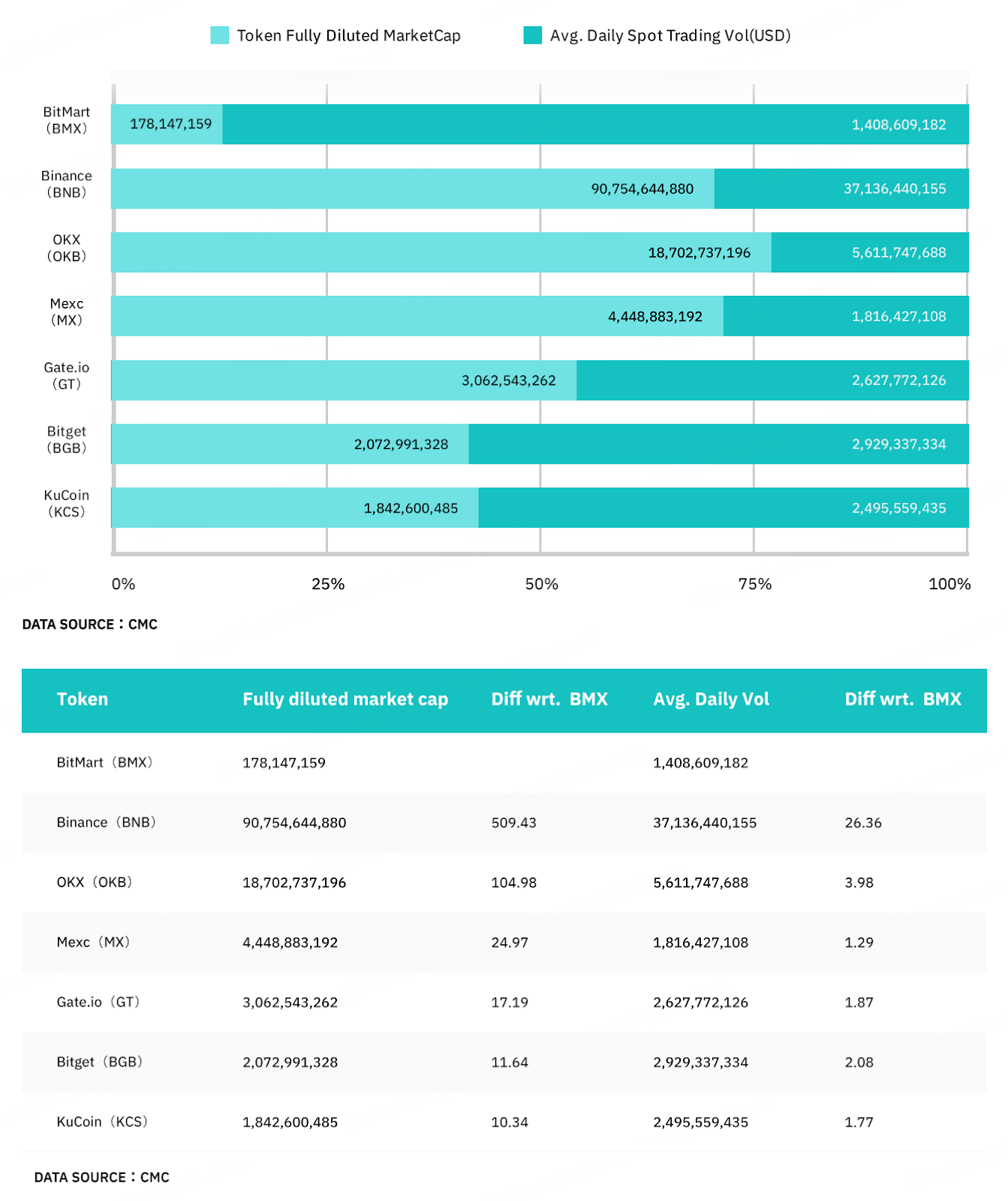

BMX HAS THE HIGHEST TRADING VOLUME TO MARKET CAP RATIO.

According to CMC data, BMX’s circulating market capital is only $178 million, significantly lower than the rest 6. BMX’s price has failed to reflect its value–it is considerably undervalued. For instance, MEXC has an average daily spot trading volume of about $1.81 billion in the past month, 29% higher than BitMart’s. However, the market capital of MX is 23.9 times that of BMX. Despite having a relatively low market capital, BMX’s market activity and demand have been rising, and the market has begun to recognize its potential value. In the last year, BMX’s market capital has increased by around 249%, with its price rising nearly 200%.

BMX V2.0 AND V3.0 UPGRADES:FURTHER EMPOWERING BMX’S VALUE

Based on BMX’s whitepaper, BitMart will launch a brand new Layer 2 blockchain, Web3 wallet, and a decentralized exchange. BMX will serve as the native asset of this network, used to pay transaction fees and smart contract fees. In addition, BMX plans to collaborate with more games, DeFi protocols, and other agreements in Q2-Q3 2024, thus applying BMX in more scenarios and becoming a consumption token, promoting ecosystem prosperity. Thereby further empowering the value of BMX.

BMX V2.0

Web3 Wallet:

BitMart’s Web3 wallet will connect centralized digital asset services with the Web3 world, with BMX as its native token. The Web3 wallet will provide a secure way to store, manage, and transfer digital assets while granting users control over their private keys.

Decentralized Exchange (DEX):

The BMX ecosystem will build a decentralized exchange by integrating liquidity and data from both CEX and DEX. BitMart aims to provide traders with a platform to help with asset price correlation assessment and formulating hedging strategies. BMX will serve as the key underlying asset and trading fee token on the DEX.

BMX V3.0

Layer 2:

The Layer 2 solutions are poised to play a crucial role in the widespread adoption of blockchain technology. The BMX ecosystem will launch a new Layer 2 blockchain. BMX will run on the new Layer 2 blockchain in the same way as ETH runs on Ethereum and be used to pay fees of transactions and smart contracts.

【SUMMARY】

BNB and OKB are the top two CEX tokens with the highest market capital. However, this results in limited growth potential for the two as they have already occupied significant market shares. On the contrary, due to its substantial price growth, BMX has drawn ample market attention.Despite its low level of market capital, we have discovered great potential through the analysis. The forthcoming upgrade plans will enhance BMX’s functionality, potentially fueling the future price and market capital.