Over the past day, Bitcoin’s price plummeted, briefly dipping below $59,000 and triggering over $100 million in long position liquidations. Intraday volatility surged by more than 70%, and the price squeeze severely impacted liquidity, significantly driving up the cost of short-term options. However, implied volatility on the back end remained relatively stable, resulting in a substantial flattening of the overall term structure. Analysts suggest that this phenomenon may be linked to the upcoming $1 billion payment to Mt. Gox creditors and Celsius’s recent repayment of $2.53 billion in debt to its users.

Source: Deribit (as of August 28, 16:00 UTC+8)

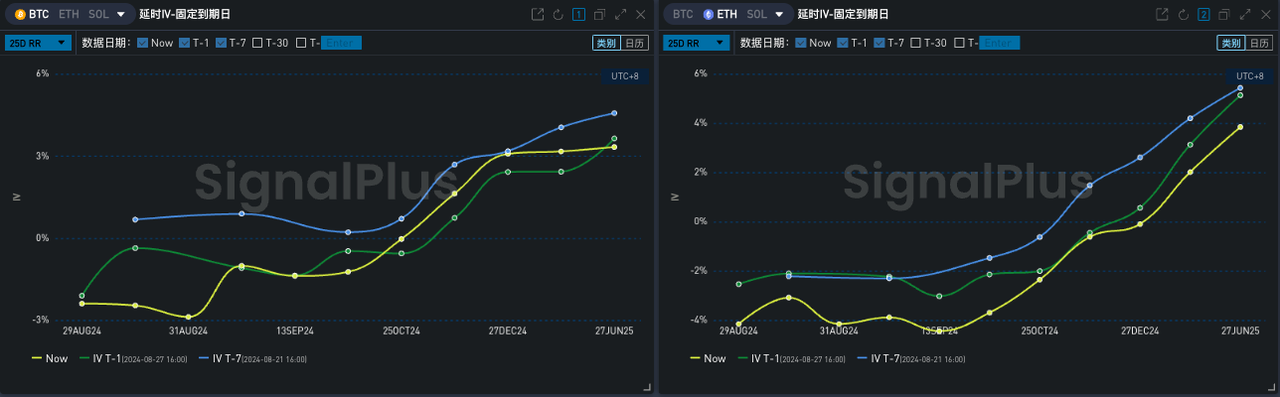

From another perspective, the sharp price fluctuations have led to a renewed rise in the tail-end Volatility Premium, with significant rebounds in both the BTC and ETH Fly indicators. However, their performance in terms of Volatility Skew has been inconsistent. Notably, the front-end risk reversal (RR) for ETH has experienced a sharp decline, driven primarily by increased demand for put options, likely influenced by recent transfer operations by the Ethereum Foundation, which continue to impact market hedging sentiment. Meanwhile, BTC’s far-end RR has seen a slight uptick during this downturn, with flow data indicating the execution of some topside call strategies.