by Donovan Choy

Five classic crypto misconceptions, refuted.

Where Regulators Are Wrong About Crypto

It’s no secret that most officials in Washington have a misguided view about crypto.

Regulators have largely failed to keep pace with broad technology changes occurring over the past 25 years, so perhaps it’s wishful thinking that they would take a more thoughtful approach to educating themselves on crypto. Nevertheless, the past few months have seen a concerted effort by American regulators to punish crypto companies and businesses that work with them. While some bad actors have been pursued, other regulator efforts betray a fundamental misunderstanding of crypto’s purpose and potential.

Here are five of their biggest complaints about crypto and why they’re still mostly wrong.

1. “Crypto has no value, it’s only for speculation”

From IMF chief Kristalina Georgieva and Elizabeth Warren to Warren Buffett, we’ve heard countless anti-crypto leaders trot out statements about crypto’s complete lack of value.

These talking points are wrong on numerous levels, most visibly in regards to how cryptocurrencies serve people in oppressive regimes and developing nations, where access to the financial system can be a luxury.

When the Turkish lira lost 40% of its value amidst hyperinflation in 2022, Turks turned to Bitcoin and USDT as a safe haven. The same is true for millions of desperate Venezuelans, Afghans, Argentinians, Ethiopians, or Nigerians whose ability to exit their hyperinflationary domestic currencies has been suppressed by Western financial sanctions or authoritarian local currency controls.

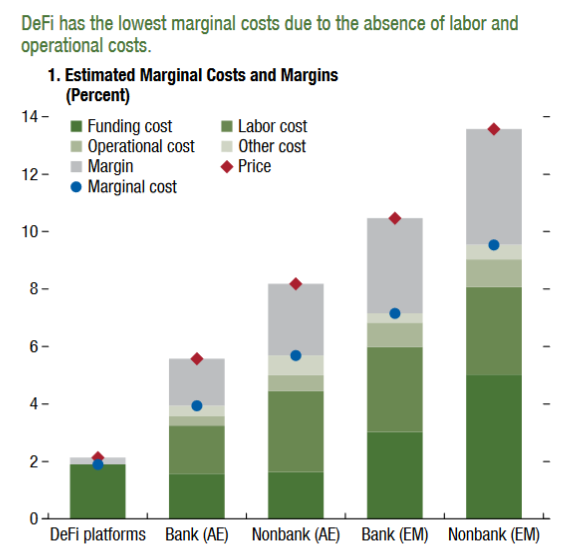

For the developed world, blockchains offer more efficient means of creating economic value that is upending traditional modes of market capitalism. Thanks to automated smart contracts and a universal ledger, one DeFi protocol with two dozen employees can perform the same work as a 200 headcount bank at a fraction of the marginal cost.

NFTs make up a ~$15 billion market that provides novel ways for artists to earn royalty fees and exercise the rights to their intellectual property. Humanitarian work, too, is evolving. When Russia went to war last year, Ukraine received at least $100 million in crypto donations within less than three weeks, a fraction of the time it would take for the same amount of money to move through political processes.

Decentralized social media and digital identity on the blockchain afford an opportunity to solve Big Tech concentration, one of the most pressing public policy problems of our time. No other sector is doing this. DAO control of more than $25 billion of value today is one of the most interesting experiments with innovation in corporate governance.

Not every one of these sectors may pan out or reach full potential, but the experimentation is pushing forward technological progress in finance. Contrary to crypto’s critics that the sector delivers no value and serves as a mere speculative instrument, the cup of value that crypto generates “runneth over”. Crypto is already solving a variety of problems today, but politicians are too blinded by partisan bias to notice.

2. “Crypto is too volatile and not a safe store-of-value”

The series of crypto crashes in 2022 continue to supply anti-crypto regulators with stronger political ammunition to double down on this line of reasoning. The recently published 2023 Annual “Economic Report of the President” by the Chair of the Council of Economic Advisers writes:

Cryptocurrencies currently experience substantial amounts of volatility, and thus are not stable stores of value. [Its] volatility means that anyone who is using bitcoins to store their savings is subject to high-volatility risk in their purchasing power… and currently are not effective alternatives to sovereign money such as the U.S. dollar.

But crypto is volatile because its access is universal. Anyone can create or trade a token, unlike stock equity that’s registration takes years of work, and trading restricted to venture capital funds and other insiders of the financial system first. If your neighborhood grocery store could issue equity, its stock too, would probably be volatile. Rather than it being a flaw, crypto’s volatility is due to its institutional egalitarianism.

Raking crypto over the coals for being an “unsafe store-of-value” might be a decent argument if our only other option, fiat, was working well. Based on CPI data, $100 in USD in 2023 has the equivalent purchasing power of $15.63 USD in 1973, effectively a loss of 84% in wealth over half a century!

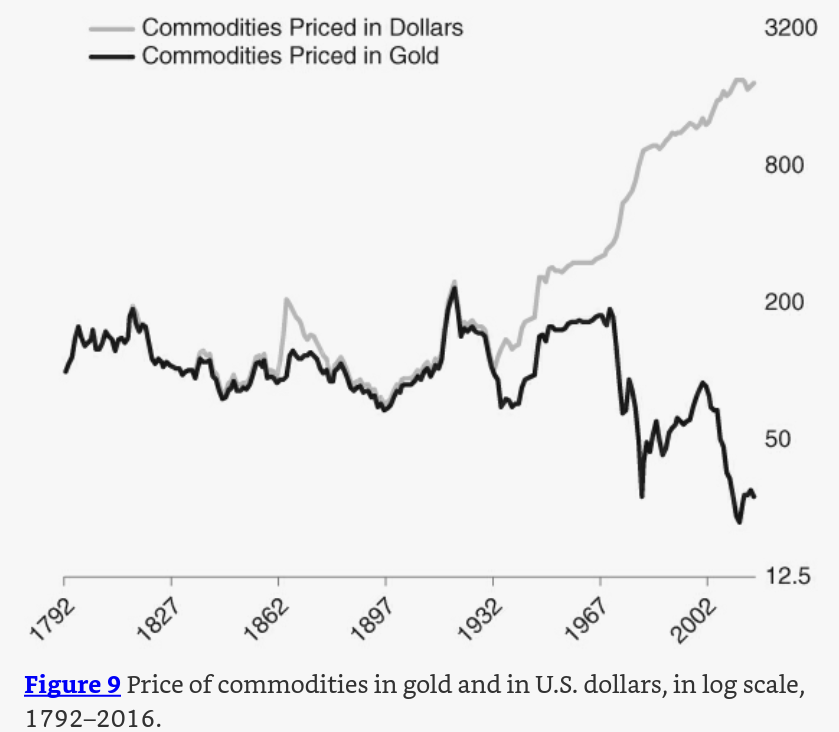

Another way to look at how poor of a store-of-value the dollar is is to compare it to a more stable value asset like gold. The US’ move off the gold standard allowed the government to heavily debase the dollar, leading to a stark divergence in the purchasing power of both assets as the below graph shows.

The moral and economic consequences of devalued fiat is far more pernicious when one considers that fiat is imposed by political monopoly on citizens and tied by law to many essential services, leaving billions with no option but to use it. Far from being a reliable store-of-value, the dollar’s hegemony imposes enormous costs on the average citizen.

That alone is sufficient reason to let the crypto experiment develop, even if it isn’t perfect. Competition is key.

3. “Crypto is scammy and needs consumer protections”

Yes, scams in crypto are very real. But scammers abound in every industry. The question is whether crypto scams deserve a harsher regulatory bar than other sectors — it’s hard to see how that might be the case.

Estimated fraud in the U.S. financial sector was $1.5 trillion in 2018, while crypto fraud last year was estimated to be a fraction of that at $1.9 billion in 2020. Scott Alexander sums it nicely: crypto isn’t so different from most other industries where the biggest companies are legitimate innovators, with dodgy projects and tokens on the long tail.

Regulators have showed hostility towards efforts to further legitimize. The SEC has repeatedly blocked institutional attempts by Grayscale, Bitwise or Ark Investment Management to apply for a Bitcoin ETF in the name of “protection of the public interest”. In a recent op-ed for The Hill, SEC Chair Gary Gensler repeated the same tired rationale for regulating tokens as securities.

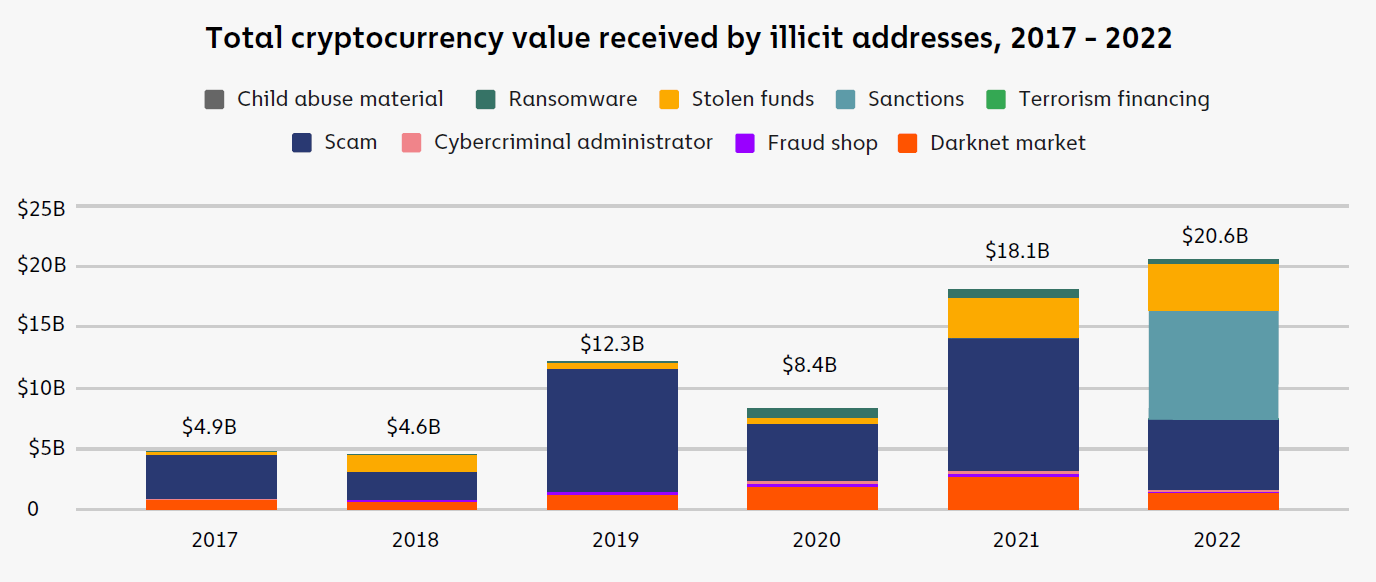

The US regulatory hostility to crypto for reasons of “consumer protection” is also deeply ironic. The average American has dozens of ways to lose their money in far riskier and legal ways. Consider commercial gambling. According to American Gaming Association data, Americans gambled at least $60.42 billion away on perfectly legal and regulated casinos and mobile gaming apps in 2022 alone. That’s ~300% more than the $20.6 billion that crypto investors lost in scams within the same year.

Despite the enormous financial risks of gambling, regulators are not feigning the same moral “consumer protection” arguments there, so why is crypto treated so differently?

4. “Crypto is great for criminals”

When all other attacks fail, regulators try to drag crypto through the dirt by tying it to the unsavory characters of the underworld. Perhaps the most forceful attempt by American regulators to do so to-date has been the Digital Asset Anti-Money Laundering Act by Senators Elizabeth Warren and Roger Marshall, a bill that would force blockchain developers, miners and validators to register as financial institutions.

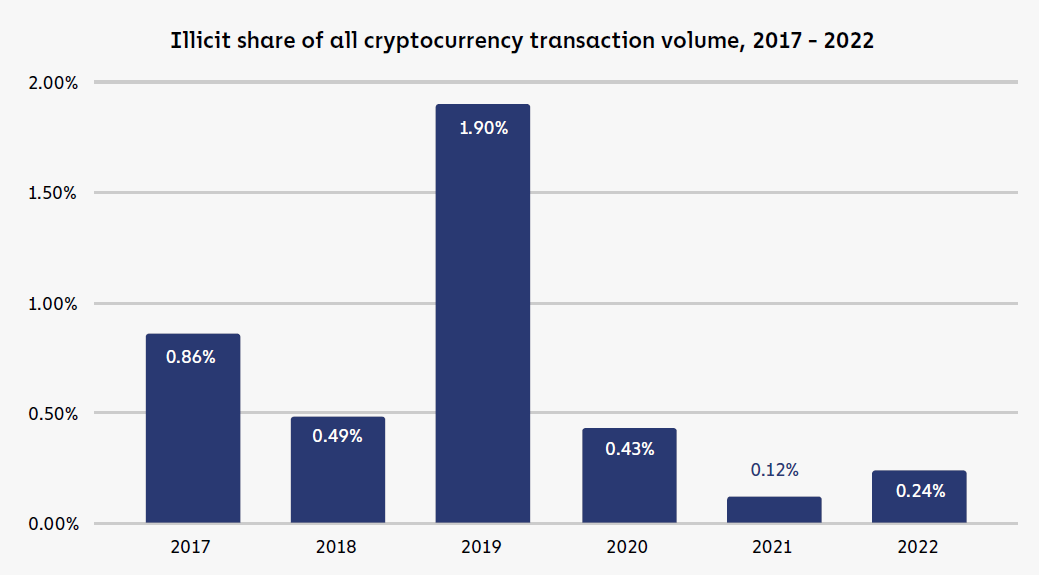

To be sure, crypto is used by some criminals. But so are banks. The pertinent question is crypto’s extent of criminal usage, and whether it justifies the frenzied reactions by Washington. Under scrutiny, these fears are once again wildly overblown. The Chainalysis 2023 Crypto Crime Report finds that crypto transaction volumes tied to “illicit activity” have never exceeded 2% in the past six years, hardly the crime-abetting tool that Elizabeth Warren makes it out to be.

When we break those numbers down further, most crypto used for “illicit means” were in scams or evasion of unjust political sanctions, not the kinds of anti-humanitarian crimes like terrorism, human trafficking or drugs that regulators frequently highlight.

The crime narrative also stems from a serious misunderstanding of how blockchains work. Public blockchains are exactly that: public. Every transaction sits on a transparent and auditable ledger, making it easily trackable – the exact opposite objective of money laundering. The US DoJ has acknowledged this on multiple occasions, writing that crypto “provides law enforcement with ample information about how, when, and how much cryptocurrency is being transferred… no subpoenas or warrants are required to obtain it.” When the DoJ arrested the perpetrators behind the $3.6 billion 2016 Bitfinex hack, it declared that “cryptocurrency is not a safe haven for criminals” because they could easily “follow money through the blockchain”.

If regulators were serious about combating money laundering, they would look inward at their own fiat currency regimes rather than fixating on crypto. By the UN’s own estimates, annual money laundering alone with the US dollar ranges from $800 billion to $2 trillion.

5. “Crypto is bad for the environment”

Finally, we turn to regulatory concerns around crypto’s carbon footprint. Thanks to the innovation of proof-of-stake consensus, these complaints have receded in recent years. But Bitcoin’s resistance to move off proof-of-work continues to provide anti-crypto politicians with an opportunity to sully crypto from a green angle.

A recent legislative hearing in the US Senate by the Committee on Environment and Public Works labeled Bitcoin mining as “harming the general public”, and would like crypto miners to report their CO2 emissions, a move that would seriously compromise the decentralization ethos of Bitcoin. It’s not just talk. New York recently moved to ban PoW mining, while President Biden’s latest 2024 budget blueprint proposes a hefty 30% energy tax on all PoW mining.

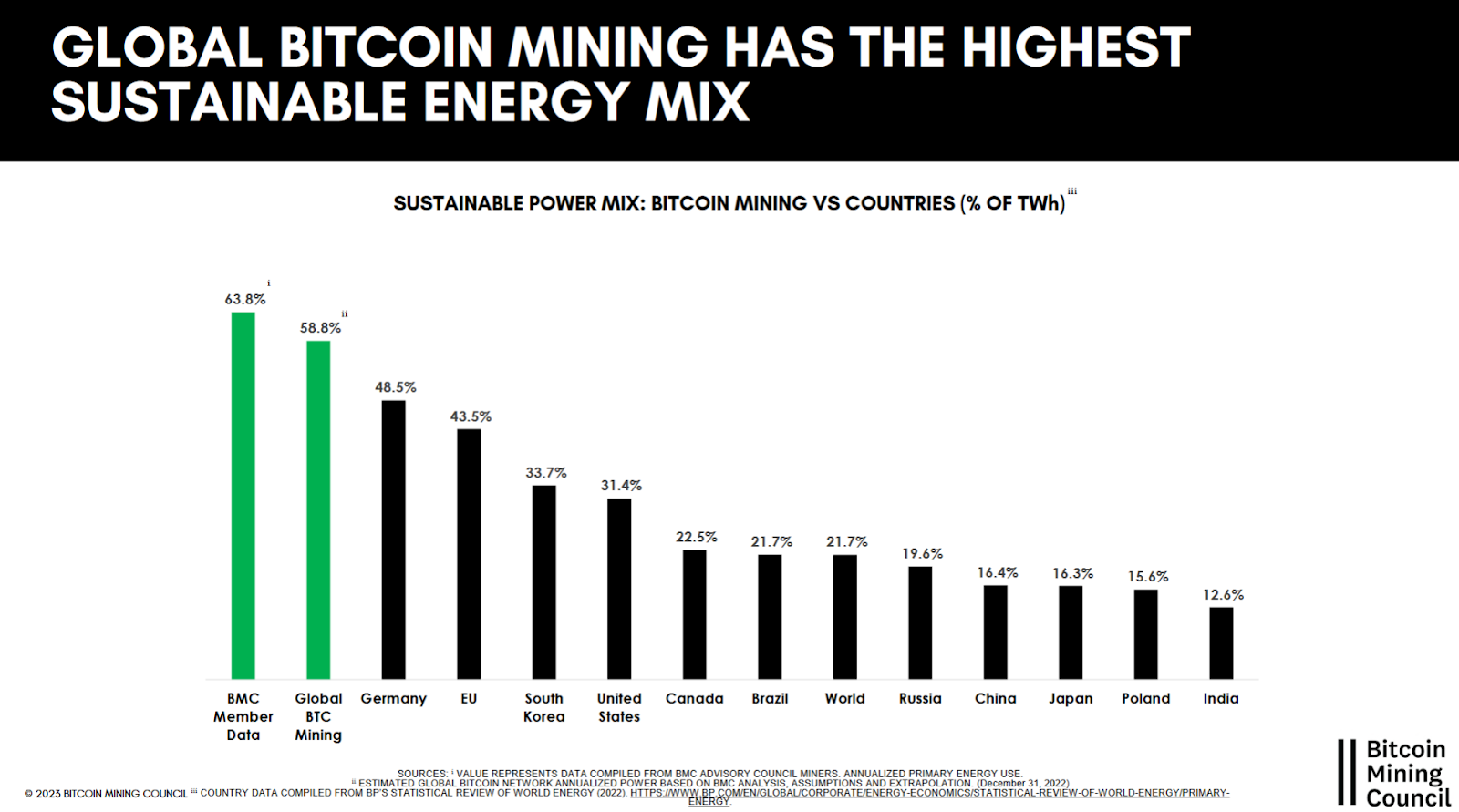

But like with most critiques of crypto, its drama falls to the ground when put into perspective. We are often told that Bitcoin’s carbon footprint is bad because it consumes more electricity (127 TWh annually) than whole nations. A CoinShares report estimates that Bitcoin is far less energy-intensive than the traditional banking system, the gold industry, or tumble dryers! Not only does Bitcoin consume less energy, its carbon footprint is also the cleanest. Bitcoin has the highest proportion of clean energy mix (59%), more so than renewable energy hubs like China and the U.S..

In an ideal world, Bitcoin would be better off on PoS consensus. In the current state, entrepreneurs are finding innovative ways to harness excess energy that would have otherwise been wasted, rendering the need for environmental regulations irrelevant.