Bitcoin Supply Trends

by Kyle Waters, Matías Andrade

Through a rising interest rate environment and broad financial markets thrashing, demand for risk assets slowed in 2022. While bitcoin (BTC) and stocks might have shared in last year’s market malaise, one asset class offers a unique perspective on the supply side of the equation. Public blockchains like Bitcoin and Ethereum offer analysts the opportunity to track supply with a much greater level of detail than is traditionally available with other financial assets.

In the aftermath of last year’s market downturn and eventful year in the digital assets space, what are some observations we can make about BTC’s supply dynamics? Using Coin Metrics’ Network Data—sourced from our Bitcoin nodes—we have identified two key on-chain trends to watch: the rise in self custody and supply freeze from long-term holders.

The Great Shift to Self Custody

The failures of centralized entities, such as Celsius and FTX, sparked a migration of coins in 2022. As non-physical assets, understanding “ownership” in the context of digital assets can be tricky and abstract at first glance. But ultimately, true ownership of crypto assets like BTC simply comes down to the control of cryptographic private keys, used to sign transactions and move funds in a crypto wallet.

Many crypto asset holders have entrusted third-party custodians such as exchanges to handle these keys on their behalf. However, in the wake of the FTX collapse, there has been a noticeable uptick in BTC balances held by small addresses, a sign of smaller holders taking custody of their keys and funds themselves.

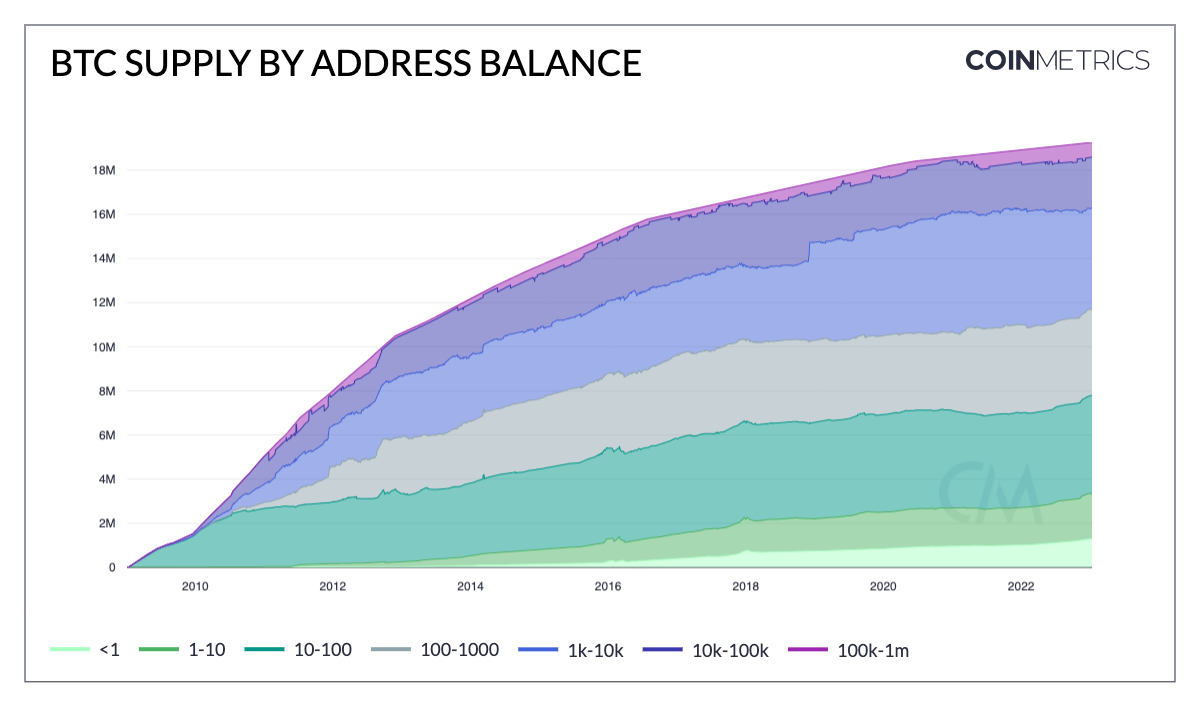

As of January 11th, 2023, 3.35M BTC is held by addresses holding under 10 BTC—a 23% rise from 2.72M a year ago.

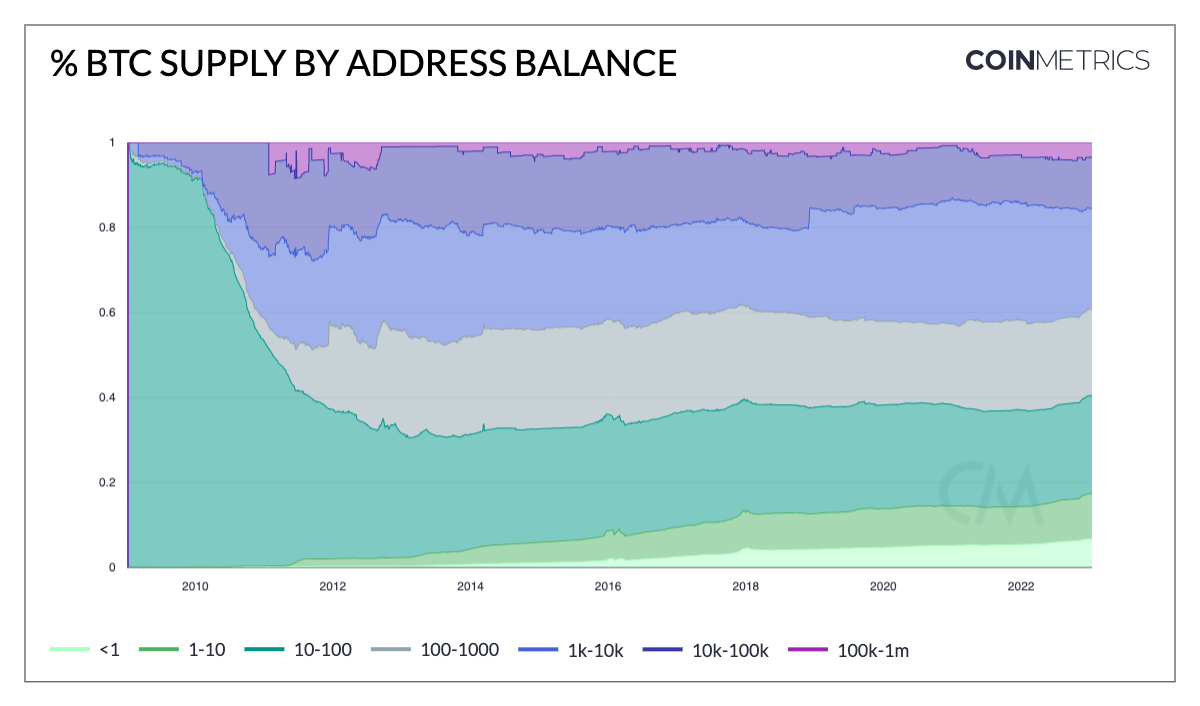

As a percentage of total BTC supply, addresses holding under 10 BTC now hold 17.4% of all supply, up from 14.4% a year ago.

In terms of addresses, the number of Bitcoin addresses holding between 0.01–1 BTC (~$210 to ~$21K) is at an all-time high of 10.5M, rising about 2M over the year and 600K just from November 1, 2022.

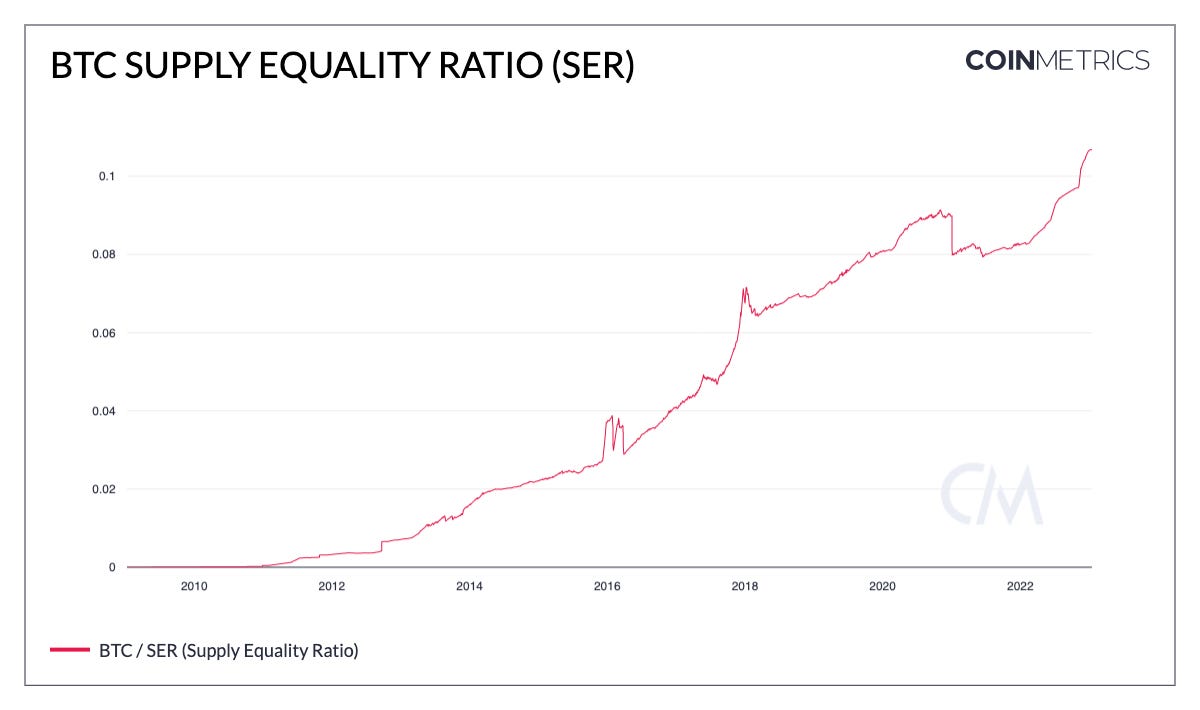

Measures of BTC’s supply dispersion have historically been misleading at the surface because of the prevalence of exchanges and custodians holding funds on the behalf of others. Bitcoin’s supply equality is a topic of endless intrigue, and the desire for self custody has improved on-chain metrics for Bitcoin’s supply equality.

The Supply Equality Ratio (SER) measures the ratio of supply held by addresses with relatively small amounts to the supply held by the top one percent of addresses. A higher SER signals a higher distribution of supply. Bitcoin’s SER is currently at an all-time high, rising sharply throughout 2022.

To be sure, the top 10% of BTC addresses still controls a large swath of supply. With the maturing custodial environment and amount of funds held on exchanges, this is still to be expected. Though, the amount of BTC controlled by these addresses has not been this low since 2012.

The move to self-custody is a welcomed development for those who encourage greater sovereignty over their assets. However, private keys need to be handled carefully, and there is no one-size-fits-all custodial solution. Mishandling private keys can lead to the worst case scenario of losing access to funds.

But as the industry matures, there are new tools and services that are being developed to help users manage and secure their digital assets. Some of these tools, such as multi-sig wallets or multiparty computation (MPC) help deliver a more robust risk profile for institutional custodians, as well as retail users. One of the large, rapidly growing niches in the digital asset industry is the role of the asset custodian, which consolidates tokens into their own wallets, using tools like multi-sig and MPC to further ensure the safety of their assets.

Conviction of Long Term Holders

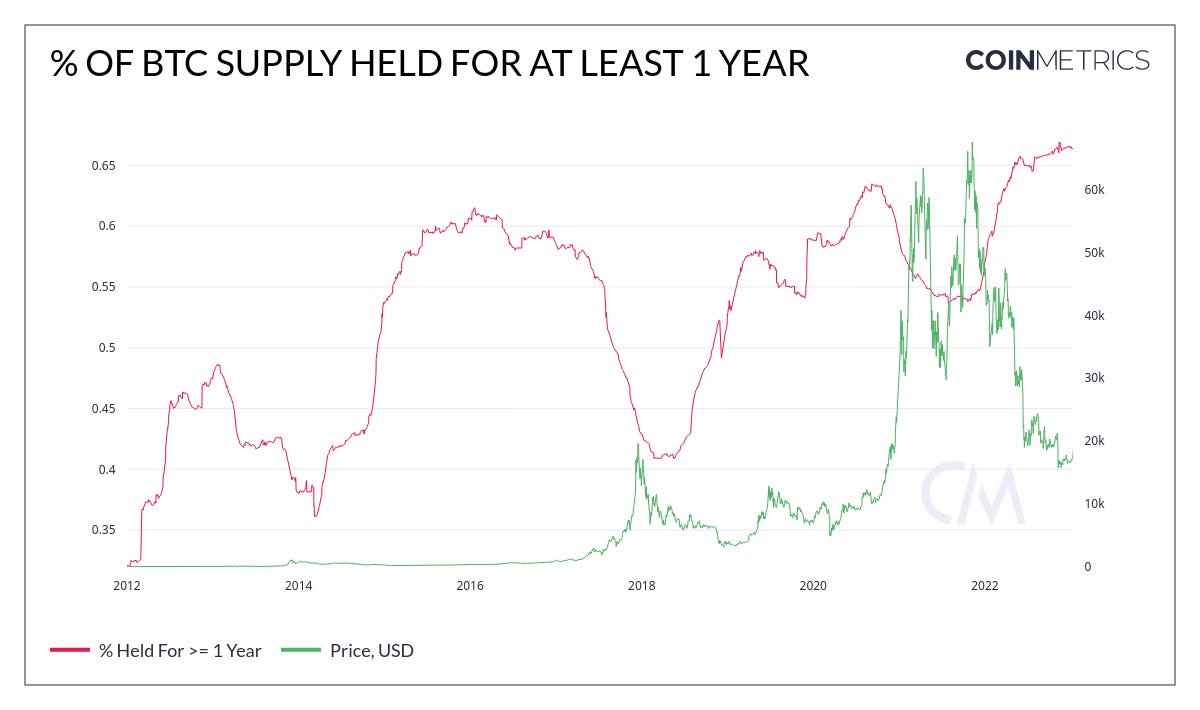

There is no question that the previous year challenged digital asset investors’ resolve. However, we are reaching a historical-high in BTC supply held for at least one year—after reaching a low near October of 2021, over 65% of total BTC supply has not changed hands for a year or longer. This is indicative of investor confidence—after exchanging hands near the top-side of the price distribution when liquidity was most favorable for distribution, this metric is consistent with long-term investors steadying their hands in expectations of further price appreciation.

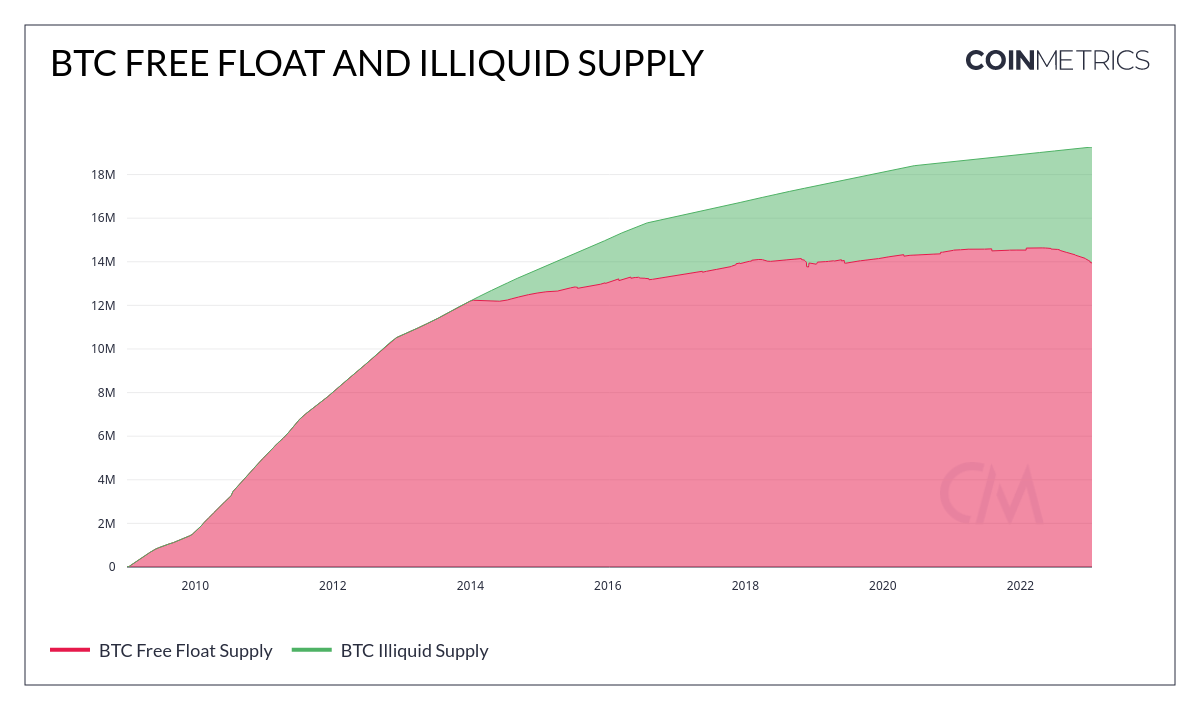

Another compelling measure of long-term investors’ conviction after the last two years’ bull-market is the increasing proportion of BTC supply absent from regular circulation, increasing our measure of Illiquid Supply. As investors remove their assets from circulation, a greater proportion of Bitcoin’s market cap is tied up in long-term investors and holders. This is consistent with the behavior of long-term holders and institutions providing digital asset services to their customers—a positive sign during a bearish market.

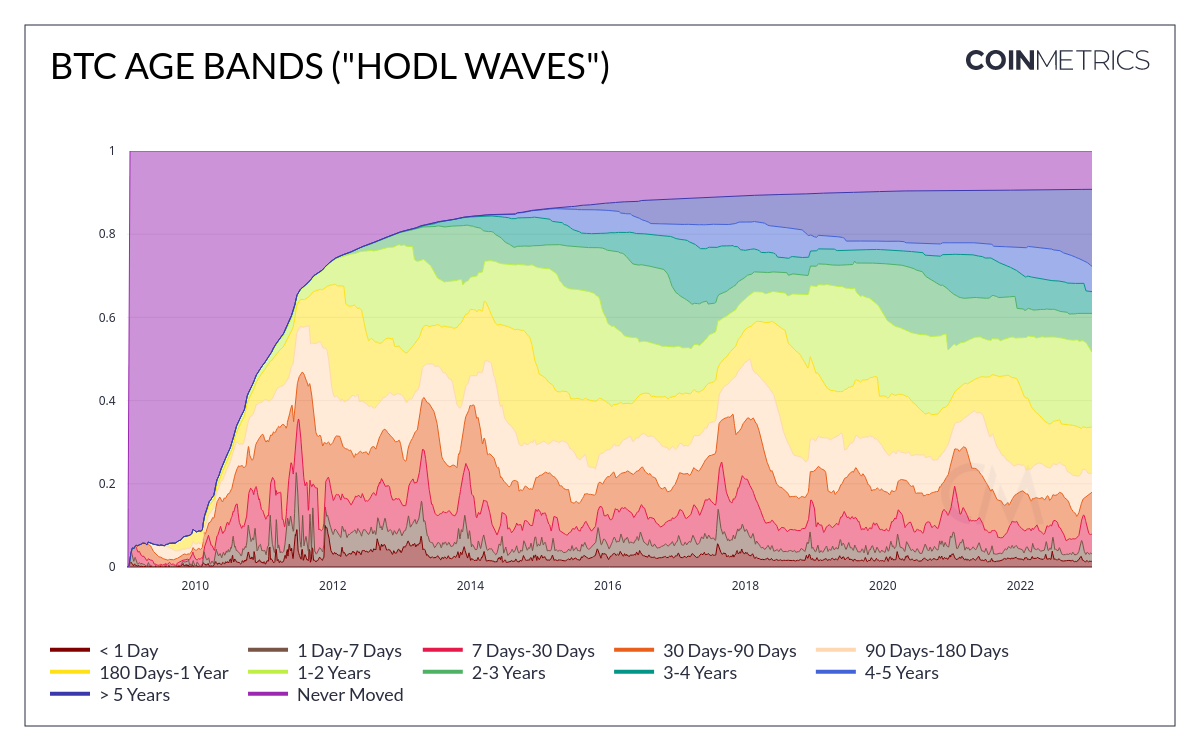

Finally, and one of the most iconic measures of on-chain investor sentiment is the Hodl Wave chart, which depicts the relative age of BTC UTXO as a measure of when they were last transacted. It is interesting to note that in previous bull runs, the amount of supply held by short-term speculative investors spikes as interest in digital assets peak in correlation with their prices, while bearish markets are distinguished by a consolidation of BTC by long-term holders. We see a trend where long-term holders (greater than one year, as indicated by the light-green band and those above it) have captured an increasing amount of the total BTC supply, with over 34% of supply held between 1–5 years. Therefore, excluding short-term holders with BTC held for under a year and unmoved (possibly lost) BTC, we can see that over 57% of BTC has been held for one year or longer.

Conclusion

There are plenty of other questions surrounding BTC supply to keep an eye on in 2022. In December, 100 BTC moved from wallets connected to QuadrigaCX, a defunct Canadian crypto exchange. There is also the specter of funds being released from the settlement of Japanese crypto exchange Mt. Gox’s 2014 insolvency in 2023. Finally, the blowouts from 2022 have likely left a portion of supply entangled in legal disputes for some time. While supply unlocks from nearly a decade ago, supply from recent events could be left untouched amid expected legal back and forth.