Abstract:

This series dives from a dual perspectives approach; by both being a practitioner in the blockchain market as well as a scholar. My goal is to convey my understanding of this market, consolidate the analytics behind my reviews, and give overall reflections on the sentiments and up to date situation of our industry.

How should we treat emerging token projects? How can retail investors rationalize the token financing of these projects in the most efficient and effective way possible? How should regulators reconcile with the industry’s potential for self-regulation through technology? How can traditional VCs max impact participate in these emerging token projects under their legal equity frameworks? As an entrepreneur, how to choose between equity and token financing to further project developments? In my review today, I want to focus on the battle between VC and token funds.

Part I

When I was starting a business, I had always encountered two soul-searching questions that all entrepreneurs face:

1. What would you do if a senior executive from Chinese tech giants like Alibaba or Tencent and founded a similar project like yours?

2. What would you do if Sequoia, IDG or Hillhouse Capital invested in your competitors?

After entering Web3, people barely ask me these questions.

The answers are simple. For (1): It doesn’t matter, we can just beat them. Neither Alibaba nor Tencent exists in Web3, and even Meta has not succeeded yet in this field. For (2): It doesn’t matter, our users across the world will not start fomo just because a well-known Chinese capital is behind the project.

I do not mean to offend any of the names mentioned above. Comparing with Web2, Web3 has further narrowed the economic moat set by geographical boundaries , and all projects are exposed to undifferentiated competitive market globally. After all, there is no such narrative to describe a project as “Binance of UK”, “Uniswap of China” or “Opensea of South Korea” in Web3.

Thus, when we talk about the battle between VCs and token funds, we should think about who can do better deal sourcing and provide better post-investment management for Web3 projects on a global scale? Although there isn’t a model answer, I believe our friends in VC who are now reading this article, may encounter some challenges when competing for projects with token funds at some point.

Crypto space is an industry driven and disseminated by influence. Almost all excellent token funds will have a “shiller”, which may seem a little depreciated before the Web2 era, but this is indeed what every project needs urgently in Web3.

Part II

Needless to say, the high annualized rate of return (IRR) and the portion of liquidated book earnings and distributions to paid in capital (DPI) that token funds earn are what makes traditional VCs feel pressured, or even envy.

In some sense, 2022 is the year of Chinese VCs officially entering Web3. I am honored to have engaged with more than 90% of VCs in China who are responsible for the Partner/VP of Web3 projects, as well as the Partners of token funds (of course, I was one of them too). The most incomprehensible part by VCs is that token funds perceive “investment” from a completely different perspective. Let’s analyze this perspective on three specific aspects.

First, Ticket size (Amount of Investment).

Token funds and traditional VCs have completely different logics in terms of profit calculations and estimations.

For traditional VCs, startups only have a very slim chance of success. As the failure rate of angel round startups is too high, so they tend to invest in Series A startups which have likely passed the most “vulnerable” period. For token funds, 90% of the crpyto projects are being invested at the “seed round” in forms of token. It only takes a very short period of time to trade tokens from primary to secondary markets. It doesn’t matter for Vcs whether the project can endure through intense competitions, they only need to achieve liquidity during the project’s “angel stage”. Most of the well-known token funds are more or less related to major exchanges. Profit can be realized if they execute their power of “post-investment management” to list the token on exchanges.

In a bull market, token funds will make the following assumptions — We will invest in a project to gain both long-term and short-term returns, and its valuation should be low. We will then build momentum together to get the project listed on exchanges swiftly.

At the TGE (Token Generate Event), the amount of token unlocked should be sufficient to pay back the investments (e.g. Some DeFi projects have a vesting schedule like this: unlock 20% at TGE, 20% quarterly vesting over one year. Therefore, as long as the market price at listing is 5 times of the investment price, the payback is realized. We can imagine, this kind of project will likely experience downward spiral a longer period after the early fomo wave.

A more important assumption is implied here – in crypto space, token funds are extremely aggressive, especially in a bull market. The expected annualized return on the underlying asset such as Bitcoin are at least 300-500%. In other words, they would expect by investing token projects at “angel stage”, at least 8 out of 10 will be profitable, and at least one of them will gain more than 10X return. Otherwise, why don’t they just buy bitcoin and hold it? Relatively, VCs are excellent enough as long as they could maintain an annualized rate of return of 20%. I have tracked well-known institutions all over the world. Among VCs that has established for over 15 years, only very few of them could achieve an average long-term return of 20% per fund — this is already satisfactory for LPs.

On the contrary, the liquidity of most token projects cannot reach the actual secondary stock market level. Frankly speaking, except for a few exchanges such as Binance, Coinbase, and Upbit, most of the exchanges do not have the depth of liquidity to enable cash out by fund-level token investors.

Therefore, instead of investing hundreds of thousands of dollars or even millions of dollars in one project but cannot cash out, it’s better to invest a smaller amount in multiple projects to allow flexible cash out.

For a long time, I believe there is a fundenmental flaw with token funds — many token funds are only focusing on primary market investment team, but do not have good secondary market sales team or post-investmnet management strategies, resulting in a lot of “wasted” return. On the other hand, most projects invested by VCs will fail, and only very few of them will be listed. Therefore, having a secondary market strategy is better than nothing, but post-investment management and exit timing are rather more important than pre-investment evaluation.

On the contrary, the fundamentals to improving the performance of a good token fund are understanding when is the best timing to realize the profits, how to set a hassle-free sales strategy from a macro perspective when facing more than hundreds listed token in the portfolio, how to efficiently transfer latest project updates from investment team to sales team, how to allocate appropriate incentives to sales team, and how to ensure having the best risk management strategy in a 24/7 market?

In fact, the return of token funds are far less than those in the earning reports — I believe when token funds report their past year earning performance to LPs in the end March, there will be significant difference comparing with the rest in May. I will discuss further below.

Second, project valuation.

When VCs first enter the crypto space, they may get confused about why a new crypto project could worth $20M, $40M, or $80M in USD?

In a straightforward way, they usually compare the valuation of equity and token of similar projects. Then, comparing with equity, is the valuation of token high or low?The answer is that, it is difficult to generalize.

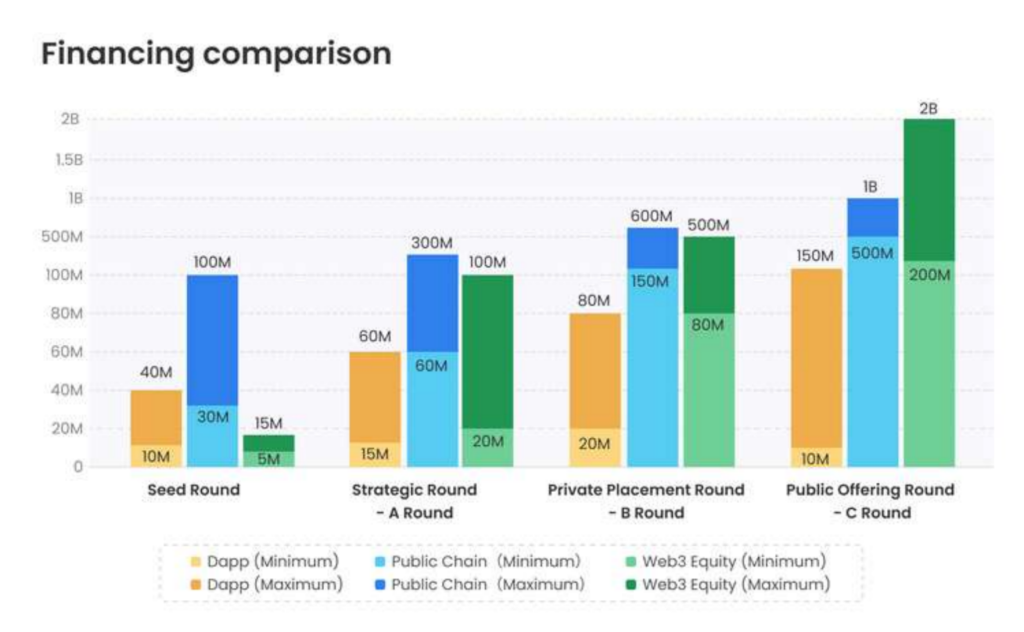

To simplify the discussion, we divide blockchain projects into three categories and let’s discuss their valuation by tiers.

Public Chain:

Seed round: $30M – $100M

Strategic round: $60M – $300M

Private placement round: $150M – $600M

Public offering round: $500M – $1B

DApp

Seed round: $10M – $40M

Strategic round: $15M – $60M

Private placement round: $20M – $80M

Public offering round: $10M -$150M

Web3 Equity:

Seed round: $5M – $15M

A round: $20M – $100M

B round: $80M – $500M

C round: $200M – $2B

The above figure shows 3 characteristics:

1. There is insignificant valuation difference between the Dapp projects’ investment rounds , and it shows a equally proportional uptrend. This is because these multiple rounds of token financing are often completed within a few months or even a few weeks. During this period, projects usually have minimum fundamental changes but with some sort of “influence premium” and “resource premium”, or even creating valuation differences in order to set priorities among investors.

2. The valuation of public chain projects is significantly higher than Dapp. Of course, from my personal point of view, there isn’t much opportunity left for public chain anymore, so I won’t elaborate further here. (Please refer to my future article《Re-discussion on Blockchain and Industrial Investment – The Golden Thirty Years》)

3. Token project has a much narrower valuation range in the entire financing cycle than equity. That being said, the valuation of token projects is significantly higher than equity at the beginning, but their last round (before listing) is significantly lower than that of later-stage equity projects. In layman’s terms, token projects are expensive the beginning and gets cheaper later.

To elaborate more on the third point, token projects demise the ability of equity project for continue financing in the future, thereby realizing the liquidity premium in advance and exchange for more rooms for growth in the secondary market with low financing ratio. We will dive into this further below. This is also the reason why Chinese token funds are not interested in NFTGo as an equity financing company. Because — according to figures above, it is impossible for token funds to understand a project with a valuation range above $100M, does not seem suitable or has no plan for token issuance. But is this really the case? In the next article, maybe you can find some hints.

However, sometimes token projects deliberately lower its primary market valuation in order to gain more traffic. As this is the only way to create enough hype for recognition from exchanges, in layman’s term, exchange more liquidity with valuation.

This is an extreme way for some marketing-oriented token projects to seize the market shares in a short term — leveraging significantly lower-than-market avearge for early rounds financing to gain support, with dozens to hundreds “investors”. For instance, a project valued at $20M but only raising 15%, but increasing investment quota to 100 to let global token funds and “community investors” quickly understand this project will definitely make profit in the short time. Also, they will promote the investment quota being scarce and everyone should hurry up to get the spot. After all, the key to bind KOLs and communities together is not how much you pay for marketing, it is to have them skin in the game, and an easy game.

Also, the price of some projects’ public offering rounds may even be down-round from the previous private rounds. Similarly, this kind of financing tactic is more of a marketing plan. Of course, there won’t be too much of token vested.

Since exchanges usually run their own ecosystem funds, projects can build a closer relationship by allowing them to participate in investment rounds and can’t be more happy to see that.

Of course, VC definitely can’t compete for this projects. Token funds often snatch for “investmnet quota” of tens of thousands of dollars , and financial investment will not get a chance. We can often see that the projects have negotiation advantages in token financing.

They usually show an attitude of “invest or not, you can’t invest more as you wish as we are fine without you”. It’s also how projects in crypto world reduce the risk of investors changing their minds by diversifying the number of investors.

Part III

Third, the number of institutional investors.

On the other hand, one thing that traditional entrepreneurs and VCs despites —why does Web3 projects always need a long list of institutional investors?

In fact, this is a necessary product of localization. When a project needs to rapidly expand the market, increase community fanbase, and search for funds with strong capability of localization in various regions. Usually, the most powerful things about these funds are local connections, resources and promotion capabilities.

For example, some names are very influential in crypto space, such as coin98 in Vietnam and 4SV in South America. However, most people in Web3 only focus on renowned names like A16Z and Paradigm, and turn a blind eye to funds in non-English speaking countries.

Similarly, comparing with IPO being the core exit strategy in stock market — the most important indicator for China’s A-share market is profitability, the most important indicator for NASDAQ listings is technology, and the most important indicator for crypto market is traffic.

When the names token funds come together, the message is very clear — this is a project widely supported by the communities around the world.

Remember, the core of Web3 project is not the company size, profit, or even technology, but it lies in the community.

Everything makes sense now — you need at least 15-20 names to build resources and social networks across the globe, plus some financial and strategic investors. It’s not surprising that Web3 projects have dozens or even hundreds of investors.

Part IV

As for long-term investors like us, we can tell whether a project is financing currency rights or equity, from the financing valuation and methods disclosed by a project, even without looking at its financing institutions.

It is an instinct.

So, thinking inversely, when we start blockchain projects ourselves, do we choose token rights or equity financing?

Or more complicatedly- first token then equity, or first equity and then token?

Let’s continue the discussion in our next chapter.