Binance’s recent audit left traders concerned. We examine why.

by Donovan Choy

This past week, Binance found itself the focus of many a crypto doomer who fear the massive CEX is following in FTX’s insolvent footsteps.

Where is the concern stemming from? Is FTX 2.0 incoming? Should crypto be worried? Let’s take these questions one at a time.

FTX blew up in November because it was an exchange that functioned more like a bank — it traded customer deposits when it wasn’t supposed to. In the wake of its shocking bankruptcy, other crypto exchanges have scrambled to signal that they weren’t doing the same shady things. They’ve aimed to do this by committing to showcasing their so-called “proof-of-reserves”.

At the center of Binance’s drama this past week is a half-baked attempt to do just that.

Binance released a 5-page audit of its reserves by the financial auditing firm Mazars — in accordance with a few “agreed-upon procedures”.

Audit shortcomings

For one, the report audits only Binance’s Bitcoin on selected chains:

For the purpose of this engagement the customers’ spot, options, margin, futures, funding, loan and earn accounts for bitcoin (“BTC”) and wrapped bitcoin (“BBTC” and “BTCB”) held on the Bitcoin, Ethereum, BNB Chain and Binance Smart Chain blockchains will be defined as the In-Scope Assets.

On top of only looking at Bitcoin, the report also looks at a select range of public addresses that were chosen by Binance:

… (Mazars will) search the ETH and/or BSC address(es) on Etherscan and BSCScan respectively to ensure that the addresses have been tagged as belonging to Binance.

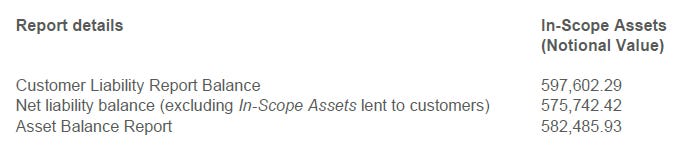

Within these narrowly-defined parameters, the Mazars report concluded with three pertinent numbers:

The first and third numbers claim that at the time of the audit (November 22), Binance holds a total of 582,486 BTC assets and customers liabilities of 597,602 BTC. This means Binance’s Bitcoin reserves are short by the 1:1 ratio mark of 15,116 BTC (2.5%).

However, Binance’s users can also borrow BTC from the exchange as part of its loan program. When we factor in these loans of 21,860 BTC (597,602 minus 575,742) into Binance’s assets, its liabilities shrink to 575,742 BTC, indicating that Binance is overcollaterized by 15,117 BTC.

So the audit concludes that Binance’s BTC funds are safu. But people are (rightfully) upset at the Mazars audit as produced as this is hardly an audit in the traditional sense.

Why only Bitcoin? What about any loans that Binance may have taken in ETH, USDT, or BNB? Those funds are omitted from the “liability” side of Binance’s balance sheet.

What about Bitcoin assets that are not on the aforementioned three chains? Any loans in wrapped Bitcoin that Binance may have borrowed on the Solana or Avalanche chain are also missing.

The whole process is a little bit like asking an auditing firm to audit a bank but by looking only at certain currencies in certain bank accounts.

Finally, there is also the problem of treating wrapped Bitcoin and Bitcoin interchangeably. This obscures the security risks involved with wrapped assets, since they are supposed to be backed by an equal underlying value in the wrapped token. Presumably, Binance would hold 1:1 for every BTCB and BBTC that it issues, but that is not known. The Mazars audit treats wrapped BTC as fundamentally secure, but Binance could be issuing more than its underlying collateral for all we know.

The Mazars report at least does one thing well: it is transparent around some of Binance’s liabilities. Most proof-of-reserves do not reveal any data on the liability side of the balance sheet. But because it neglects all non-BTC assets, it comes up woefully short on proving a complete picture of Binance’s financial health.

Binance has said that it would reveal more information on its other assets in the near future. But for now, the audit only proves a slice of Binance’s reserves, rather than a comprehensive view.

All the ruckus led to Mazars announcing December 16 that it was halting audit work for Binance and its other crypto clients including Kucoin and Crypto.com.

How is Binance actually doing?

There are rampant rumors and people are panicking, but things still appear pretty business-as-usual at Binance, which announced Monday that its US arm had reached a $1B deal to acquire Voyager’s assets.

So, really, what’s the situation looking like at Binance?

Binance saw massive outflows in the past week worth billions, with $4.27B withdrawn on December 14 alone. This was partially sparked by on-chain data of prominent TradFi players like Jump and Wintermute pulling out their funds from Binance on the 12th.

While those are some eye popping numbers, let’s take it in context. Binance’s total proof-of-reserves reported elsewhere – not to be confused with the Mazars report that audited only Bitcoin – show a quantity of ~$55B as of December 19, down from ~$70B before the current PR crisis commenced.

If Binance was nearing the end, it would show on its ETH and stablecoin asset outflows depleting to near-zero, as was the case with FTX.

While sizeable outflows are occurring as users look to avoid any chances of an FTX 2.0, on-chain data is telling a different story. Binance’s stablecoin and ETH reserves are still sitting at ~22B and ~5M respectively.

A significant contributor to FTX’s troubles was also in the use of its own FTT token for collateralizing loans. FTX was an exchange that functioned as a bank: it traded customer’s deposits when it wasn’t supposed to. It was a house of cards built on trust and reliance in itself, rather than other more financially robust collateral like U.S. Treasuries, BTC or ETH.

If Binance’s business was similarly built on its own BNB token, we may have more cause for concern. Thankfully, only ~10% of Binance’s reserves are made up of BNB, which is about the same as most other crypto exchanges.

BNB also differs from FTT in one important respect: its utility. FTT was used for trading discounts on FTX, but if the public believes your exchange is impending insolvency, FTT is not going to help. BNB on the other hand, is also an asset that is used for validating and paying transaction fees on the second largest L1 chain today by TVL: BNB Chain.

BNB saw a price plummet to $221 on December 17, but has since recovered 11% to $241 today.

In closing…

All of these indicators show that while Binance is experiencing something of a bank run, the situation is certainly not as precarious as Twitter chatter is playing it up to be.

“Bank run” may not even be the appropriate term here because Binance is an exchange, not a bank, and as long as it holds all customer’s deposits 1:1 in accordance to their terms of service (unlike FTX), no one would lose a cent even if every user wanted to take their money out.

The problem is that we don’t know that definitively, and that really gets at the heart of why holding your crypto on a centralized exchange will never be as secure as holding it on your own non-custodial wallet.