by Matías Andrade and Kyle Waters

Decentralized finance (DeFi) is a rapidly growing application of blockchain technology that aims to provide financial services, such as access to crypto-collateralized loans, yield on investments, and derivative products, with billions of dollars worth of cryptocurrency locked up in various DeFi protocols. At the heart of these protocols are DeFi tokens, which are digital assets that are used to facilitate governance and economic incentives within these protocols. In this issue of the State of The Network, we take a look at the latest developments of tokens in the DeFi space, including market dynamics, supply statistics and measures of adoption.

A Year to Build

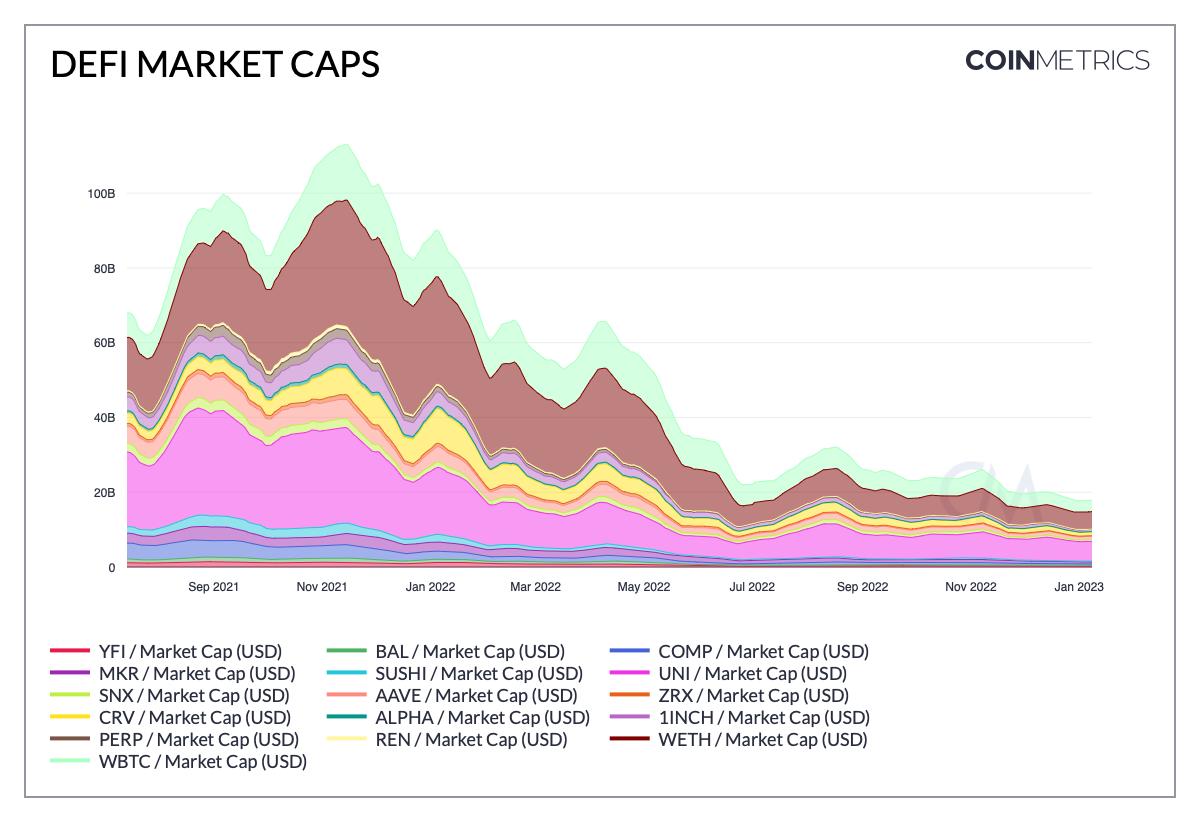

As shown in the chart, the aggregate market cap for DeFi tokens has experienced a significant decline over the past few months. This decline can be attributed to a number of factors, including rising interest rates which introduce competition against yield-bearing DeFi products, overall macroeconomic uncertainty and tech rut, and recent unwinding of malinvestments within the crypto space.

Despite the recent decline, the DeFi ecosystem has seen tremendous growth over the past few years. In January 2020, the overall DeFi ecosystem was worth under $2 billion. Today, it is worth around $18 billion, although it is still below its peak valuation of around $100 billion. The previous bull-run likely helped spur investment in protocol development and, in spite of the decline, had a huge impact in helping fund ecosystem development. It is important to note that while the aggregate market cap may fluctuate, the underlying innovation and infrastructure development spurred by these lofty valuations is likely to create persistent value among some (but probably not all) of the projects.

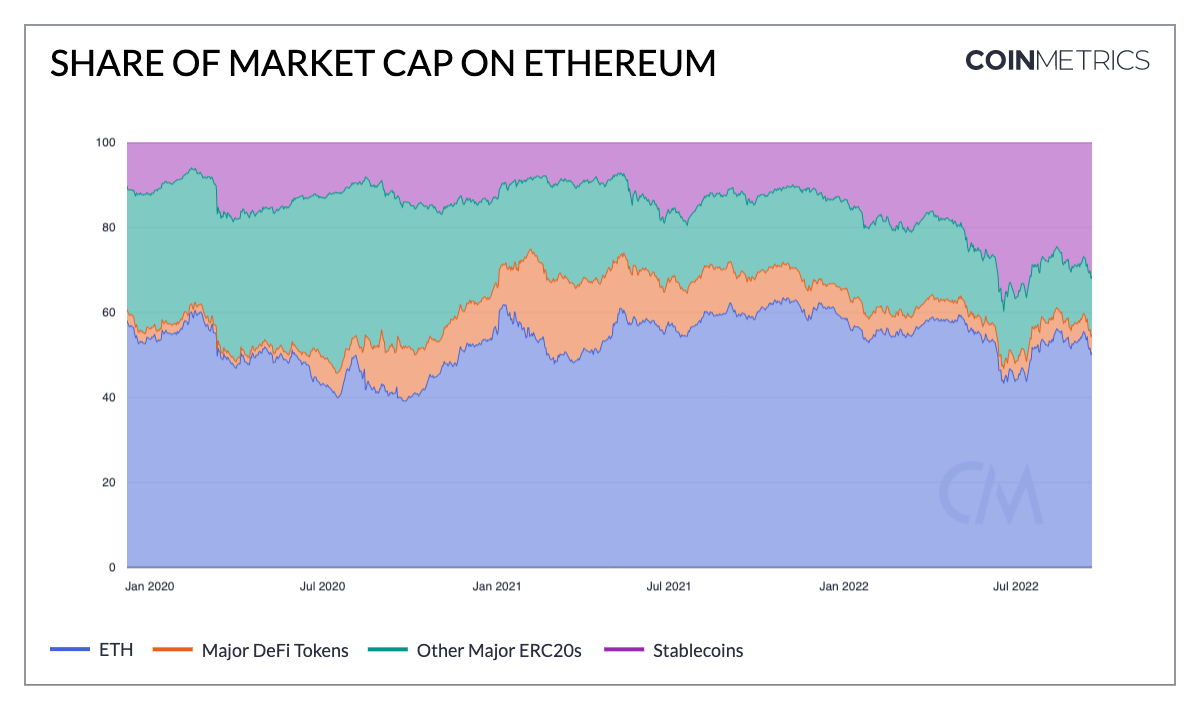

One of the interesting dynamics playing out on the Ethereum blockchain—the smart contract platform with the most significant amount of DeFi activity—is the weight of the tokens’ market cap compared to the base-layer asset, ETH. As a consequence of recent months’ market performance, savvy investors have parked their wealth in stablecoins while eschewing riskier assets, as seen in the increasing share of total value that stablecoins command. During the 2021 spring bull market, DeFi tokens’ share of market capitalization bulged on Ethereum.

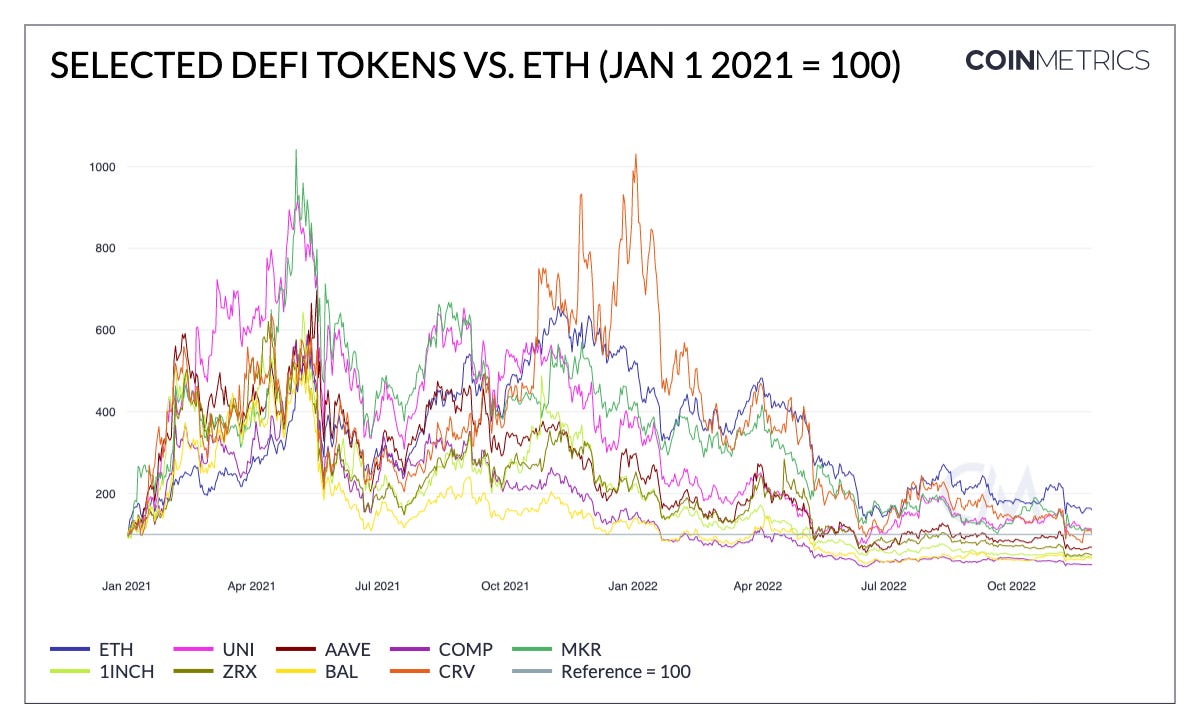

In spite of this development, it is also worth noting the relative performance of ETH compared to various DeFi tokens. It is clear that investors’ risk appetite has tightened considerably, but as they reconsider their holdings they are growing more selective as well. So far, ETH has held its value more effectively than DeFi tokens.

Supply Side Tokenomics

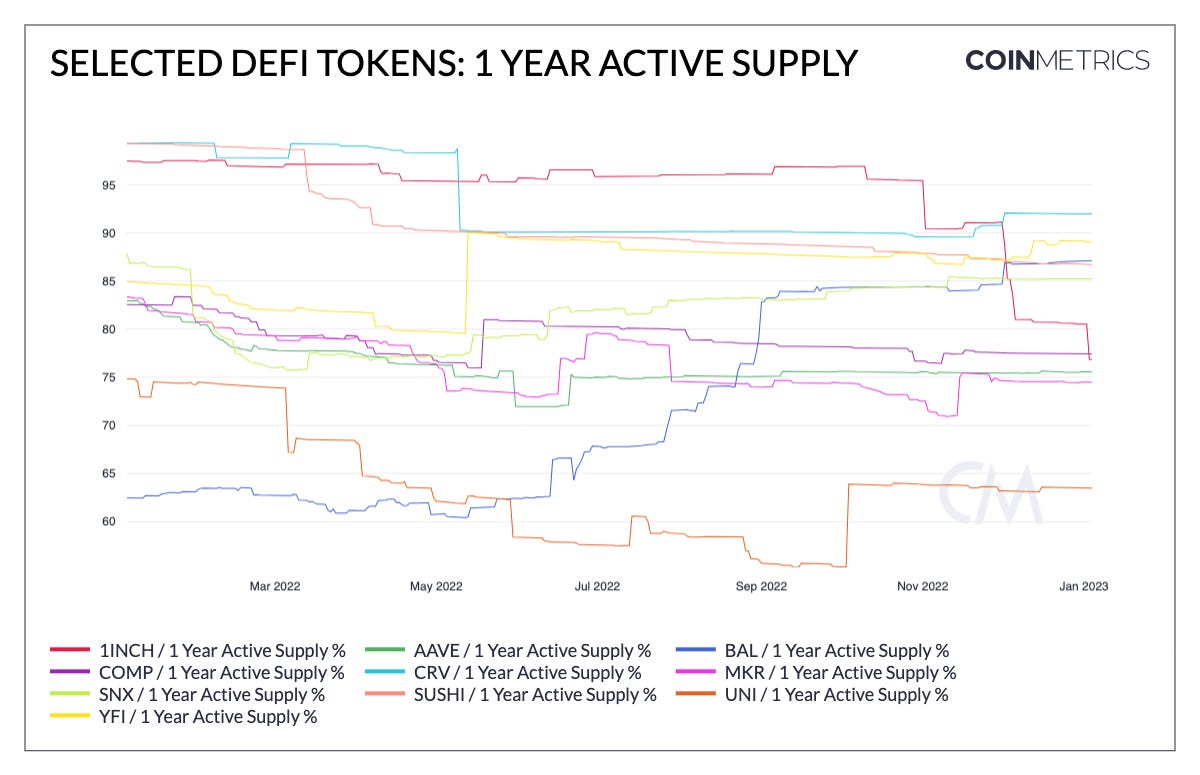

One of the most important issues to consider when judging the relative performance of DeFi tokens, and particularly when making inferences about future performance, is the relative amount of tokens held by treasuries, developers or early investors. While most tokens release most of the supply to be traded in the market freely, most also have a lock-up period where certain investors are given early or discounted access to purchase a token with the condition that these tokens must be held for a minimum period. Depending on the amount of tokens that are held in lock-up, upon release they can have a significant impact on the markets, especially if token owners wish to realize their returns by liquidating their holdings. With this in mind, we can take a look at our 1–year active supply percentage metric to estimate the percentage of supply that isn’t actively traded.

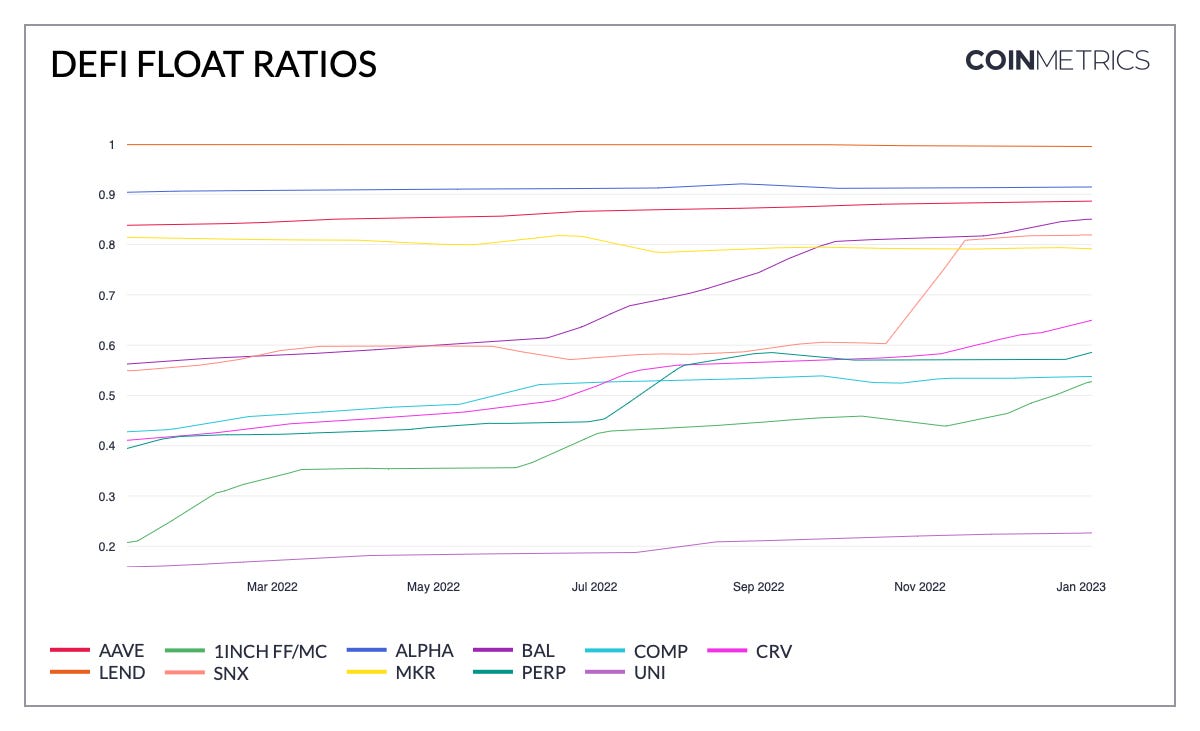

We can also consider a measure of these effects that we borrow from traditional financial markets called the float ratio. This ratio refers to the share of assets that is available for trade on the market, and can help one estimate the potential future risk of a large asset holder from liquidating their tokens, causing significant volatility and price swings.

In the context of DeFi tokens, the float ratio can be used to protect one’s investments from volatility by identifying tokens with a low float ratio. It is interesting to note that, while the float ratios and 1–year active supply charts are different interpretations of the same idea, they are mostly in agreement with each other. We can see a relatively low 1–year active supply as well as a low-float ratio for UNI, lending coherence to this idea. UNI has a 4-year release schedule for the 1B UNI tokens minted in the genesis of the token in 2020. Similarly, we can see that float ratios have been trending higher during the last year, which is indicative of supply being progressively unlocked.

Adoption

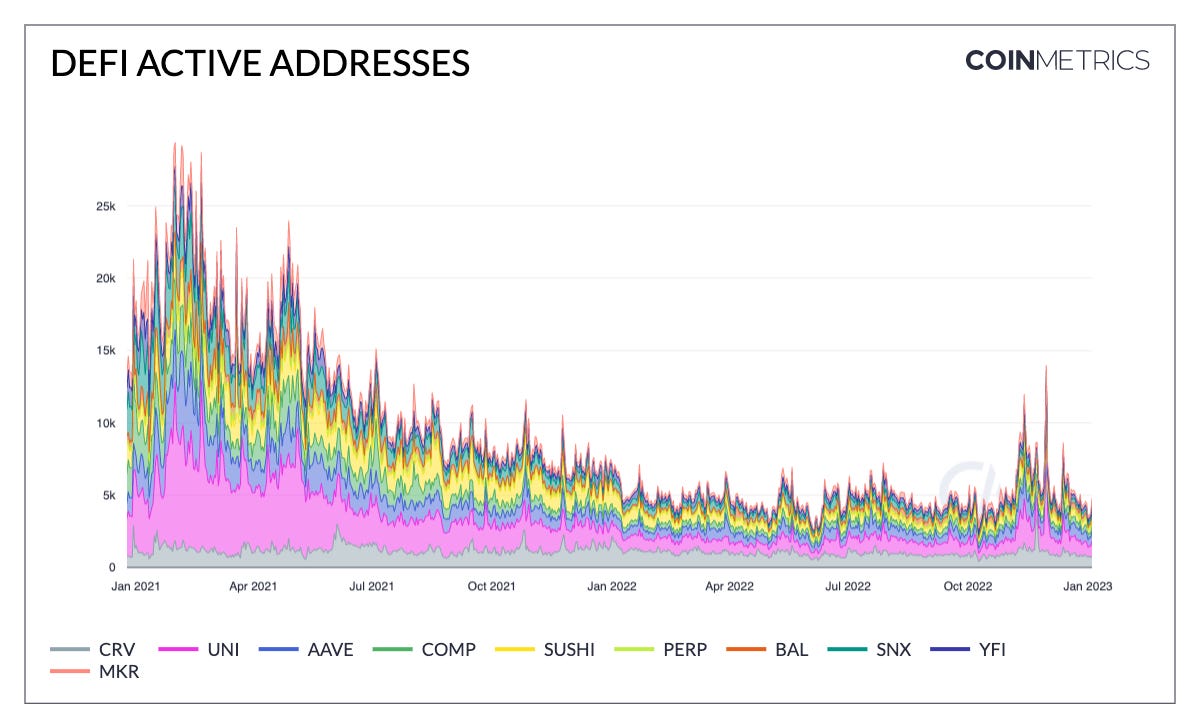

The number of addresses interacting with DeFi tokens has fallen since the beginning of 2021. However, when measuring the adoption of DeFi applications, looking at active addresses interacting with DeFi tokens is a very rough proxy. This is because protocol usage is generally separate from protocol governance (usually in the form of a decentralized autonomous organization, or DAO). For example, a user of Uniswap does not need to own the UNI token to interact with the Uniswap smart contract and trade assets (unless UNI is a one of the tokens being traded).

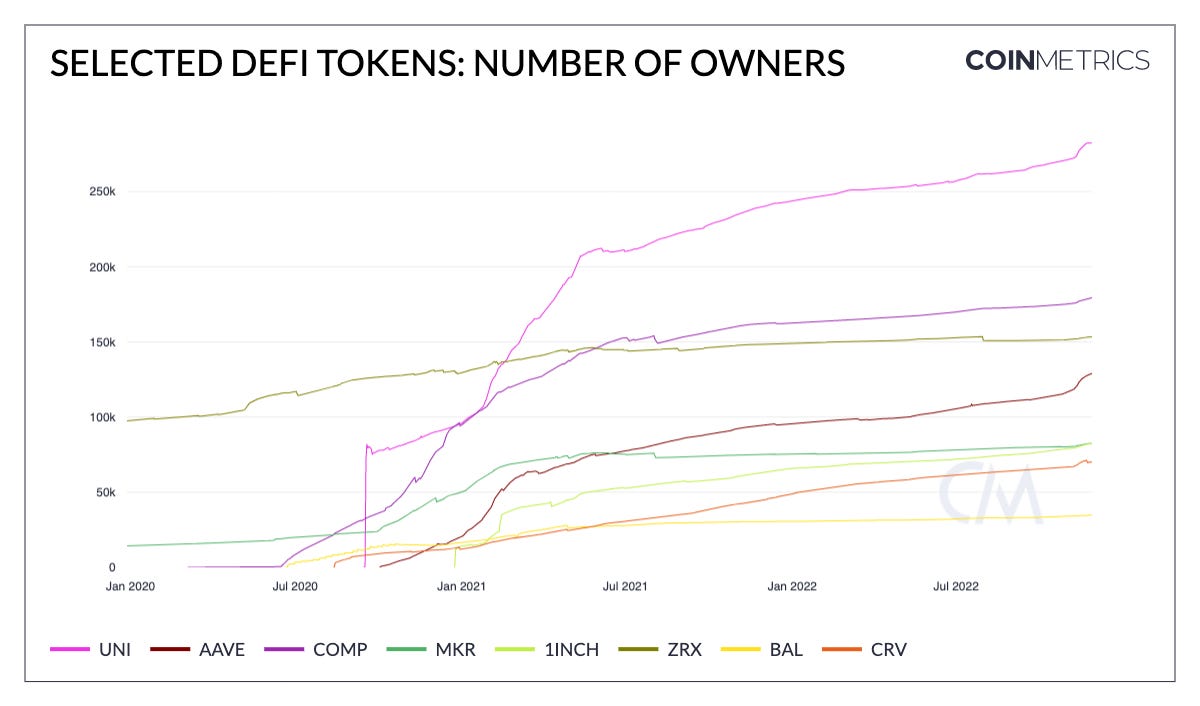

It is also helpful to look at the number of owners of DeFi tokens to assess adoption and interest. A decentralized owner base can be advantageous in the context of a DAO because it implies a broader voter base with diversity of perspectives over issues. Most tokens showed a slow upward trend in owners on-chain in 2022, before jumping markedly in November as many users moved their tokens off exchange. Uniswap’s UNI remains one of the most popular DeFi tokens, with over 280K unique addresses owning the token. UNI was famously first distributed via an airdrop to historical protocol users in September 2020, and has grown its owner base since.

Conclusion

As an emerging industry with uncertain cash flows, DeFi tokens suffered through a period of investor de-risking in 2022. There are some possible catalysts that might help reboot interest in DeFi tokens in 2023. Firstly, some projects might continue to experiment with underlying token dynamics. Last year, the MakerDAO community debated revisions to the dynamics of the MKR token including the addition of a staking mechanism. On the regulatory side, any movement towards clarification on the issue of token securities vs. commodities would be welcomed progress in the industry, including the potential adoption of new disclosure frameworks for token issuers.

With the acute awareness of centralized agents’ recent failures, expectations are high for DeFi to excel in 2023. Indeed, the CMBI Decentralized Finance Sector Even index (CMBIDFIE)—an even-weighted basket of all assets in the decentralized finance sector of datonomy—is up 14% to start the new year.

DeFi observers will be watching token performance closely—but, as we’ve described in this piece, it is important to detach DeFi tokens from the underlying adoption of the protocols. With DeFi token data, it is possible to paint a broad picture of the space but more fine-tuned protocol data is needed for proper due diligence and adoption analysis. To this end, we look forward to expanding our breadth of DeFi analyses in 2023.